-

Ascent Named Best Places to Work in Fintech 2026Ascent, a leading provider of innovative financial products and student support services that enable more students to access education and achieve academic and economic success, has been named one of the 2026 Best Places to Work in Fintech, an awards program created in 2017 by Arizent and Best Companies Group. This annual survey and awards program recognizes the top employers in the financial technology industry. Honorees operate across a wide range of financial services sectors, including banking, mortgages, insurance, payments and financial advisory. To be eligible, companies must provide technology products or services that support financial services delivery, have been in business for at least one year, and employ at least 15 people in the U.S. "Each year, the Best Places to Work in Financial Technology offers a glimpse into the practices of fintechs whose employees rate their workplaces highly," said Penny Crosman, executive editor of technology at American Banker. "This year, employees appear to value remote work and schedule flexibility above all else, at a time when many traditional financial firms have enforced strict return-to-work policies." Companies from across the United States entered a two-part survey process to determine Arizent’s Best Places to Work in Fintech. The first part consisted of evaluating each nominated company's workplace policies, practices, philosophy, systems and demographics. The second part consisted of an employee survey to measure the employee experience. The combined scores determined the top companies and the final ranking. Best Companies Group managed the overall registration and survey process, analyzed the data and determined the final ranking. “We’re proud to have built a workplace where employees feel trusted, supported, and genuinely connected to the work they do,” said Emily Skoubo, Director of Human Resources at Ascent. “This recognition reflects the collaborative culture our team has created together and our continued focus on providing an environment where people can grow, contribute, and feel valued.” For more information on Arizent’s Best Places to Work in Fintech program, including full eligibility criteria, visit www.BestPlacestoWorkFinTech.com or contact Penny Crosman at [email protected]. About Ascent Ascent is a leading provider of innovative financial products and wrap-around student support services that enable more students to access education and achieve academic and economic success. Everything Ascent offers is designed by leading industry professionals and with advanced technology and innovation to increase every student’s ability to plan, pay, and succeed. Ascent’s rare Outcomes-based Loan provides funding to credit-invisible borrowers who generally do not benefit from traditional credit. Ascent products also include: Cosigned Loans, Solo Loans, Career Loans, Parent Loans, Graduate Loans, Access Loans, Enterprise Loans and Impact Loans.

Ascent Named Best Places to Work in Fintech 2026Ascent, a leading provider of innovative financial products and student support services that enable more students to access education and achieve academic and economic success, has been named one of the 2026 Best Places to Work in Fintech, an awards program created in 2017 by Arizent and Best Companies Group. This annual survey and awards program recognizes the top employers in the financial technology industry. Honorees operate across a wide range of financial services sectors, including banking, mortgages, insurance, payments and financial advisory. To be eligible, companies must provide technology products or services that support financial services delivery, have been in business for at least one year, and employ at least 15 people in the U.S. "Each year, the Best Places to Work in Financial Technology offers a glimpse into the practices of fintechs whose employees rate their workplaces highly," said Penny Crosman, executive editor of technology at American Banker. "This year, employees appear to value remote work and schedule flexibility above all else, at a time when many traditional financial firms have enforced strict return-to-work policies." Companies from across the United States entered a two-part survey process to determine Arizent’s Best Places to Work in Fintech. The first part consisted of evaluating each nominated company's workplace policies, practices, philosophy, systems and demographics. The second part consisted of an employee survey to measure the employee experience. The combined scores determined the top companies and the final ranking. Best Companies Group managed the overall registration and survey process, analyzed the data and determined the final ranking. “We’re proud to have built a workplace where employees feel trusted, supported, and genuinely connected to the work they do,” said Emily Skoubo, Director of Human Resources at Ascent. “This recognition reflects the collaborative culture our team has created together and our continued focus on providing an environment where people can grow, contribute, and feel valued.” For more information on Arizent’s Best Places to Work in Fintech program, including full eligibility criteria, visit www.BestPlacestoWorkFinTech.com or contact Penny Crosman at [email protected]. About Ascent Ascent is a leading provider of innovative financial products and wrap-around student support services that enable more students to access education and achieve academic and economic success. Everything Ascent offers is designed by leading industry professionals and with advanced technology and innovation to increase every student’s ability to plan, pay, and succeed. Ascent’s rare Outcomes-based Loan provides funding to credit-invisible borrowers who generally do not benefit from traditional credit. Ascent products also include: Cosigned Loans, Solo Loans, Career Loans, Parent Loans, Graduate Loans, Access Loans, Enterprise Loans and Impact Loans. -

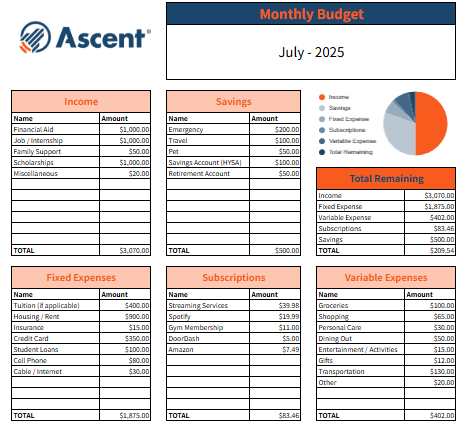

Smart Money Moves: The Ultimate Guide to Budgeting for College StudentsCollege is an exciting time to explore, grow, and gain independence—including getting comfortable with money. Budgeting might sound intimidating, but it’s really just a way to make sure your money supports the life you want to live. With the right strategy and tools, any student can manage money effectively, reduce stress, and set themselves up for future financial success. Why Budgeting is Crucial for College Students Budgeting gives you control over your money, even when it feels like you don’t have much. It helps you cover essentials, avoid debt, and still enjoy life on and off campus. Whether you’re managing a part-time income or student loans, a budget keeps you organized, prepared for surprises, and builds good habits for life after college. Step 1: Understand Your Finances – Creating a Realistic Budget Before you can build a budget that works, you need to understand where your money is coming from and where it’s going. Taking the time to get clear on your income, expenses, and savings goals is the foundation of smart money management. Track Your Income Sources: Before you can plan how to spend or save, it’s important to know how much money you have coming in. Identifying all your income sources will give you a clear starting point for your budget. Financial aid (grants, scholarships, loans) Job income Family support or allowance Know Your Expenses: Prioritize Needs vs. Wants Once you understand your income, the next step is to track your spending. Breaking your expenses into needs and wants can help you make smarter decisions about where your money goes. Fixed Expenses (Needs): Tuition, rent, utilities, insurance, credit cards, bills Variable Expenses (Wants): Food, entertainment, supplies, clothing, personal care Savings: Fund Your Future Saving might not feel urgent right now, but it’s one of the most powerful habits you can start. Even small contributions help you build a financial safety net and encourage long-term habits that will support your goals well beyond college. Savings Accounts: Emergency Fund, travel expenses, pet care High Yield Savings Account: Have higher interest rates and enable faster growth of your savings Retirement Plans (401k, Roth IRA): Tax-advantaged savings plans to help grow savings over time for retirement expenses Use a Budgeting Method Choosing a budgeting method gives structure to your financial plan and helps you stay consistent with your spending, savings, and goals. 50/30/20 Rule: 50% needs, 30% wants, 20% savings/debt repayment This rule helps individuals manage their finances by prioritizing essential expenses, discretionary spending, and long-term financial goals. 50% Needs: Essential expenses you must pay to live and work 30% Wants: Non-essential but enhance quality of life 20% Savings: Strengthening your financial future Envelope Method: Physical or digital envelopes for each category Determine budget categories Set monthly budget for each Withdraw cash and fill envelopes Spend only from those envelopes Step 2: Save Where You Can Once you’ve built a basic budget, the next step is finding ways to stretch your dollars further. The good news? As a college student, there are tons of easy ways to save without sacrificing fun or convenience. From student discounts to smart spending habits, a few small changes can make a big difference. Here’s how to make the most of what you have. Student discounts: Show student ID at restaurants, shopping stores, movie theaters, etc. Apps to get student discounts: UNiDAYS, Student Beans Textbooks: Rent, buy used, library copies Food: Cook at home, use meal plans wisely, avoid daily coffee shop habits, check supermarket ads for deals Transportation: Use public transit, bike, or carpool Most colleges provide free transportation passes Entertainment: Attend free campus events, share streaming accounts Step 3: Prepare for the Unexpected Even the best budgets can be thrown off by surprise expenses. Whether it’s a last-minute trip home, a medical bill, or an extra textbook you didn’t plan for, life happens. That’s why it’s important to build a financial cushion that helps you handle the unexpected without stress—or debt. Here’s how to stay prepared and protect your budget. Build an Emergency Fund: Aim for a $500 goal to start Plan for Irregular Expenses: Books, holidays, trips, birthdays, medical expenses Step 4: Use Tools to Stay on Track Creating a budget is a great start—but staying on track takes a little help. Thankfully, there are plenty of simple tools that can keep you organized and consistent, even on your busiest days. Whether you prefer apps, spreadsheets, or calendar reminders, the right tools can make managing your money quicker, easier, and less stressful. Let’s look at a few that can help you stay in control. Spreadsheets: Custom Google Sheets or Excel Download Ascent’s Student Budgeting Sheet here! Banking Tools: Auto alerts for low balance, spending summaries Calendar Reminders: For bill due dates and budget check-ins Block specific date/time on your calendar to sort your finances Common Budgeting Mistakes to Avoid Even with the best intentions, it’s easy to slip up. Being aware of common budgeting mistakes can help you stay on track and avoid unnecessary stress. Here are a few pitfalls to watch out for: Underestimating daily spending: Every purchase adds up! Not reviewing your budget monthly: Adjust for changes Overlooking one-time costs: Move-in costs, graduation fees, etc. Relying on your credit cards: Make sure you have the funds to pay them back Building Healthy Financial Habits Good budgeting isn’t just about numbers—it’s about building habits that support your goals over time. With a few consistent practices, managing your money can become second nature. Here’s how to turn smart choices into lasting habits: Track every dollar: Even small purchases add up Set time aside time to review your account weekly Set your goals: avoid overdrafts, reduce credit card use Stick to your budget for 3 months? Treat yourself (responsibly)! Final Thoughts Budgeting is an essential skill that can make your college experience less stressful and more empowering. It’s not about getting everything right the first time—it’s about starting small, staying flexible, and learning from your experiences. With a little effort and consistency, you’ll build habits that not only help you thrive in college but also set you up for long-term financial success.

Smart Money Moves: The Ultimate Guide to Budgeting for College StudentsCollege is an exciting time to explore, grow, and gain independence—including getting comfortable with money. Budgeting might sound intimidating, but it’s really just a way to make sure your money supports the life you want to live. With the right strategy and tools, any student can manage money effectively, reduce stress, and set themselves up for future financial success. Why Budgeting is Crucial for College Students Budgeting gives you control over your money, even when it feels like you don’t have much. It helps you cover essentials, avoid debt, and still enjoy life on and off campus. Whether you’re managing a part-time income or student loans, a budget keeps you organized, prepared for surprises, and builds good habits for life after college. Step 1: Understand Your Finances – Creating a Realistic Budget Before you can build a budget that works, you need to understand where your money is coming from and where it’s going. Taking the time to get clear on your income, expenses, and savings goals is the foundation of smart money management. Track Your Income Sources: Before you can plan how to spend or save, it’s important to know how much money you have coming in. Identifying all your income sources will give you a clear starting point for your budget. Financial aid (grants, scholarships, loans) Job income Family support or allowance Know Your Expenses: Prioritize Needs vs. Wants Once you understand your income, the next step is to track your spending. Breaking your expenses into needs and wants can help you make smarter decisions about where your money goes. Fixed Expenses (Needs): Tuition, rent, utilities, insurance, credit cards, bills Variable Expenses (Wants): Food, entertainment, supplies, clothing, personal care Savings: Fund Your Future Saving might not feel urgent right now, but it’s one of the most powerful habits you can start. Even small contributions help you build a financial safety net and encourage long-term habits that will support your goals well beyond college. Savings Accounts: Emergency Fund, travel expenses, pet care High Yield Savings Account: Have higher interest rates and enable faster growth of your savings Retirement Plans (401k, Roth IRA): Tax-advantaged savings plans to help grow savings over time for retirement expenses Use a Budgeting Method Choosing a budgeting method gives structure to your financial plan and helps you stay consistent with your spending, savings, and goals. 50/30/20 Rule: 50% needs, 30% wants, 20% savings/debt repayment This rule helps individuals manage their finances by prioritizing essential expenses, discretionary spending, and long-term financial goals. 50% Needs: Essential expenses you must pay to live and work 30% Wants: Non-essential but enhance quality of life 20% Savings: Strengthening your financial future Envelope Method: Physical or digital envelopes for each category Determine budget categories Set monthly budget for each Withdraw cash and fill envelopes Spend only from those envelopes Step 2: Save Where You Can Once you’ve built a basic budget, the next step is finding ways to stretch your dollars further. The good news? As a college student, there are tons of easy ways to save without sacrificing fun or convenience. From student discounts to smart spending habits, a few small changes can make a big difference. Here’s how to make the most of what you have. Student discounts: Show student ID at restaurants, shopping stores, movie theaters, etc. Apps to get student discounts: UNiDAYS, Student Beans Textbooks: Rent, buy used, library copies Food: Cook at home, use meal plans wisely, avoid daily coffee shop habits, check supermarket ads for deals Transportation: Use public transit, bike, or carpool Most colleges provide free transportation passes Entertainment: Attend free campus events, share streaming accounts Step 3: Prepare for the Unexpected Even the best budgets can be thrown off by surprise expenses. Whether it’s a last-minute trip home, a medical bill, or an extra textbook you didn’t plan for, life happens. That’s why it’s important to build a financial cushion that helps you handle the unexpected without stress—or debt. Here’s how to stay prepared and protect your budget. Build an Emergency Fund: Aim for a $500 goal to start Plan for Irregular Expenses: Books, holidays, trips, birthdays, medical expenses Step 4: Use Tools to Stay on Track Creating a budget is a great start—but staying on track takes a little help. Thankfully, there are plenty of simple tools that can keep you organized and consistent, even on your busiest days. Whether you prefer apps, spreadsheets, or calendar reminders, the right tools can make managing your money quicker, easier, and less stressful. Let’s look at a few that can help you stay in control. Spreadsheets: Custom Google Sheets or Excel Download Ascent’s Student Budgeting Sheet here! Banking Tools: Auto alerts for low balance, spending summaries Calendar Reminders: For bill due dates and budget check-ins Block specific date/time on your calendar to sort your finances Common Budgeting Mistakes to Avoid Even with the best intentions, it’s easy to slip up. Being aware of common budgeting mistakes can help you stay on track and avoid unnecessary stress. Here are a few pitfalls to watch out for: Underestimating daily spending: Every purchase adds up! Not reviewing your budget monthly: Adjust for changes Overlooking one-time costs: Move-in costs, graduation fees, etc. Relying on your credit cards: Make sure you have the funds to pay them back Building Healthy Financial Habits Good budgeting isn’t just about numbers—it’s about building habits that support your goals over time. With a few consistent practices, managing your money can become second nature. Here’s how to turn smart choices into lasting habits: Track every dollar: Even small purchases add up Set time aside time to review your account weekly Set your goals: avoid overdrafts, reduce credit card use Stick to your budget for 3 months? Treat yourself (responsibly)! Final Thoughts Budgeting is an essential skill that can make your college experience less stressful and more empowering. It’s not about getting everything right the first time—it’s about starting small, staying flexible, and learning from your experiences. With a little effort and consistency, you’ll build habits that not only help you thrive in college but also set you up for long-term financial success. -

How Graduate Students Can Adjust to Grad Plus Loan NewsStudent loans are a hot topic these days, and for good reason. There have been massive shake ups in education under the Trump administration, from the proposed dissolution of the U.S. Department of Education to sweeping changes to how student loans could be administered and managed in the future. The potential impact of these proposed changes is not limited to undergrads and future college students and their families. With the cost of a master's degree averaging between $44,000 to $71,000, many graduate students also rely on federal student aid, such as Grad PLUS loans, to fund their continuing education. If you’re a grad student, you're probably wondering how these changes might impact your future and your ability to pay for graduate school. Let's walk through the potential changes and explore some alternative financial aid options, should Grad PLUS loans become unavailable. Key Takeaways Grad PLUS loans are a type of federal loan offered by the U.S. Department of Education that can cover up to the full cost of attending graduate school. Republican lawmakers have proposed changes to the federal student loan programs that administer graduate loans, including reduced caps on unsubsidized loans and eliminating Grad PLUS loans altogether. If these proposed changes become law, current graduate students will likely be grandfathered in, but future graduate students may need to seek alternative sources of financial aid. Scholarships, fellowships, need-based grants, graduate assistantships, work-study programs, federal unsubsidized loans, and private student loans are alternative funding options graduate students can consider. What Are Grad PLUS Loans? Grad PLUS loans are a type of Direct PLUS loan specifically for eligible graduate and professional students. These credit-based federal loans are offered by the U.S. Department of Education and allow students to borrow up to the full cost of attendance (graduate tuition, fees, and living expenses) minus any other financial aid received. They come with a fixed interest rate and borrower protections, and they’re a popular option because federal unsubsidized loans often don’t cover the full cost of advanced degrees. According to recent federal data, Grad PLUS loans account for a significant portion of graduate student debt. As many as 1.8 million borrowers hold these loans, totaling up to $117.2 billion. This has caught the attention of some policymakers, who are starting to take a closer look at these loans. The high borrowing limits and growing debt load have sparked increased scrutiny of Grad PLUS loans, especially as discussions around the student loan crisis and reforms have intensified. Policymakers are raising the possibility of reform—or even elimination—as ways to reduce the overall burden of graduate-level debt. Will the Grad PLUS Loan Program be Cut? Discussions around eliminating the Grad PLUS loan program have gained traction on Capitol Hill, especially among Republican lawmakers who want to rein in federal spending on graduate education. These lawmakers argue that unlimited borrowing under the program inflates the cost of graduate degrees and places an undue debt burden on students. They’ve introduced bills such as the College Cost Reduction Act of 2024, which proposed eliminating Direct PLUS loans. While it didn’t pass, similar themes in legislation have been introduced in 2025. The Graduate Opportunity and Affordable Loans Act, introduced by Alabama Senator Tommy Tuberville in January 2025, proposes to eliminate the ability of graduate and professional students to receive Direct PLUS loans and sets the aggregate limit on unsubsidized loans to $65,000 for a graduate student. While the bill was referred to the Committee on Health, Education, Labor, and Pensions, it has yet to proceed. Even though neither bill targeting Grad PLUS loans has passed, they each signal lawmakers’ appetite for reforming graduate lending. That means potential changes to how students finance advanced degrees. What Grad PLUS Loan News Means for Borrowers As policymakers debate the future of federal student aid, Grad PLUS loans are undeniably on the chopping block. For current and prospective graduate students, that adds another layer of uncertainty to an already stressful financial climate. Rising tuition costs and fewer affordable borrowing options could leave many students scrambling to cover expenses. Finding student loans for graduate school, including from private lenders, will become more necessary for students who’ve exhausted free financial aid options. Current Grad PLUS Borrowers Students already enrolled or recent graduates with active Grad PLUS loans probably won’t see major changes, at least in the short term. If Congress eliminates the program, existing borrowers will likely be “grandfathered” in, meaning they can keep their current loans and repayment terms as they are. The uncertainty around the Grad PLUS loan 2024-2025 cycle could complicate financial planning for those midway through multi-year programs. If you’re in either of these groups, pay close attention to Grad PLUS loan news developments and start researching backup funding strategies in case future borrowing under Grad PLUS is capped or phased out. Future Grad PLUS Borrowers Future graduate students might be at bigger risk of losing out on Grad PLUS funding. If this federal loan program is eliminated, students may need to rely more heavily on private loans to finance their education. While private loans are just as effective at funding advanced degrees and may offer additional benefits like access to career readiness tools, they may also come with tighter credit requirements, variable interest rates, and other considerations—so it is important to compare your options. This shift from federal to private loans could disproportionately impact students with limited or poor credit histories. As a result, some may delay graduate studies, choose lower-cost institutions, or seek employer-sponsored education benefits. Others may turn to part-time enrollment or work full-time when studying, lengthening the time needed to complete a degree. If you’re thinking about attending grad school, now is the time to start preparing: Compare graduate program costs and consider how you might pay for your desired program if Grad PLUS loans go away. Research and apply for graduate scholarships, fellowships, and other grants. To do so, you’ll need to complete the Free Application for Federal Student Aid (FAFSA) every year. Apply for graduate assistantships or federal work-study programs. Availability of these programs may impact your school choice. Look into employer education benefits to help cover the cost of graduate school. Take steps to build a strong credit profile, research private loan terms, and prepare to borrow if you still need to cover costs. Ascent Is Here to Help We know that paying for grad school is an important concern for all students, and that Grad PLUS loans have been a vital resource. Even if they go away, however, there are still options. Try to be selective about your desired program, pursue all your options for free financial aid, and take your time comparing lenders for private student loans. Ascent can help you find the right loan terms and interest rate to support your graduate education, but we’re here for you beyond borrowing. Our resources for students and families offer guidance about paying for school, better budgeting, career-readiness, and more. Amid ongoing student loan changes, Ascent remains committed to empowering student success and financial wellness. FAQs What alternative loan options are available if the Grad PLUS ends? If Grad PLUS loans are phased out, future graduate students should first explore financial aid that doesn’t need to be repaid such as scholarships, fellowships, grants, graduate assistantships, work-study programs, and employer tuition reimbursement programs. If there are any gaps in funding, graduate students should consider federal unsubsidized loans and private student loans. Can private student loans cover the full cost of grad school? In many cases, private student loans can cover the full cost of attending graduate school, from tuition and fees to living expenses. Private loans have unique eligibility and loan limits determined by the lender, and they usually depend on your credit history or income. That makes planning and comparing loans from different providers a necessity. Will Grad PLUS loans be forgiven? Grad PLUS loans may be eligible for forgiveness under existing federal programs like the Public Service Loan Forgiveness (PSLF) or Income-Driven Repayment (IDR) plan forgiveness, provided you meet the necessary qualifications. However, there’s no separate forgiveness initiative specifically for Grad PLUS loans at this time.

How Graduate Students Can Adjust to Grad Plus Loan NewsStudent loans are a hot topic these days, and for good reason. There have been massive shake ups in education under the Trump administration, from the proposed dissolution of the U.S. Department of Education to sweeping changes to how student loans could be administered and managed in the future. The potential impact of these proposed changes is not limited to undergrads and future college students and their families. With the cost of a master's degree averaging between $44,000 to $71,000, many graduate students also rely on federal student aid, such as Grad PLUS loans, to fund their continuing education. If you’re a grad student, you're probably wondering how these changes might impact your future and your ability to pay for graduate school. Let's walk through the potential changes and explore some alternative financial aid options, should Grad PLUS loans become unavailable. Key Takeaways Grad PLUS loans are a type of federal loan offered by the U.S. Department of Education that can cover up to the full cost of attending graduate school. Republican lawmakers have proposed changes to the federal student loan programs that administer graduate loans, including reduced caps on unsubsidized loans and eliminating Grad PLUS loans altogether. If these proposed changes become law, current graduate students will likely be grandfathered in, but future graduate students may need to seek alternative sources of financial aid. Scholarships, fellowships, need-based grants, graduate assistantships, work-study programs, federal unsubsidized loans, and private student loans are alternative funding options graduate students can consider. What Are Grad PLUS Loans? Grad PLUS loans are a type of Direct PLUS loan specifically for eligible graduate and professional students. These credit-based federal loans are offered by the U.S. Department of Education and allow students to borrow up to the full cost of attendance (graduate tuition, fees, and living expenses) minus any other financial aid received. They come with a fixed interest rate and borrower protections, and they’re a popular option because federal unsubsidized loans often don’t cover the full cost of advanced degrees. According to recent federal data, Grad PLUS loans account for a significant portion of graduate student debt. As many as 1.8 million borrowers hold these loans, totaling up to $117.2 billion. This has caught the attention of some policymakers, who are starting to take a closer look at these loans. The high borrowing limits and growing debt load have sparked increased scrutiny of Grad PLUS loans, especially as discussions around the student loan crisis and reforms have intensified. Policymakers are raising the possibility of reform—or even elimination—as ways to reduce the overall burden of graduate-level debt. Will the Grad PLUS Loan Program be Cut? Discussions around eliminating the Grad PLUS loan program have gained traction on Capitol Hill, especially among Republican lawmakers who want to rein in federal spending on graduate education. These lawmakers argue that unlimited borrowing under the program inflates the cost of graduate degrees and places an undue debt burden on students. They’ve introduced bills such as the College Cost Reduction Act of 2024, which proposed eliminating Direct PLUS loans. While it didn’t pass, similar themes in legislation have been introduced in 2025. The Graduate Opportunity and Affordable Loans Act, introduced by Alabama Senator Tommy Tuberville in January 2025, proposes to eliminate the ability of graduate and professional students to receive Direct PLUS loans and sets the aggregate limit on unsubsidized loans to $65,000 for a graduate student. While the bill was referred to the Committee on Health, Education, Labor, and Pensions, it has yet to proceed. Even though neither bill targeting Grad PLUS loans has passed, they each signal lawmakers’ appetite for reforming graduate lending. That means potential changes to how students finance advanced degrees. What Grad PLUS Loan News Means for Borrowers As policymakers debate the future of federal student aid, Grad PLUS loans are undeniably on the chopping block. For current and prospective graduate students, that adds another layer of uncertainty to an already stressful financial climate. Rising tuition costs and fewer affordable borrowing options could leave many students scrambling to cover expenses. Finding student loans for graduate school, including from private lenders, will become more necessary for students who’ve exhausted free financial aid options. Current Grad PLUS Borrowers Students already enrolled or recent graduates with active Grad PLUS loans probably won’t see major changes, at least in the short term. If Congress eliminates the program, existing borrowers will likely be “grandfathered” in, meaning they can keep their current loans and repayment terms as they are. The uncertainty around the Grad PLUS loan 2024-2025 cycle could complicate financial planning for those midway through multi-year programs. If you’re in either of these groups, pay close attention to Grad PLUS loan news developments and start researching backup funding strategies in case future borrowing under Grad PLUS is capped or phased out. Future Grad PLUS Borrowers Future graduate students might be at bigger risk of losing out on Grad PLUS funding. If this federal loan program is eliminated, students may need to rely more heavily on private loans to finance their education. While private loans are just as effective at funding advanced degrees and may offer additional benefits like access to career readiness tools, they may also come with tighter credit requirements, variable interest rates, and other considerations—so it is important to compare your options. This shift from federal to private loans could disproportionately impact students with limited or poor credit histories. As a result, some may delay graduate studies, choose lower-cost institutions, or seek employer-sponsored education benefits. Others may turn to part-time enrollment or work full-time when studying, lengthening the time needed to complete a degree. If you’re thinking about attending grad school, now is the time to start preparing: Compare graduate program costs and consider how you might pay for your desired program if Grad PLUS loans go away. Research and apply for graduate scholarships, fellowships, and other grants. To do so, you’ll need to complete the Free Application for Federal Student Aid (FAFSA) every year. Apply for graduate assistantships or federal work-study programs. Availability of these programs may impact your school choice. Look into employer education benefits to help cover the cost of graduate school. Take steps to build a strong credit profile, research private loan terms, and prepare to borrow if you still need to cover costs. Ascent Is Here to Help We know that paying for grad school is an important concern for all students, and that Grad PLUS loans have been a vital resource. Even if they go away, however, there are still options. Try to be selective about your desired program, pursue all your options for free financial aid, and take your time comparing lenders for private student loans. Ascent can help you find the right loan terms and interest rate to support your graduate education, but we’re here for you beyond borrowing. Our resources for students and families offer guidance about paying for school, better budgeting, career-readiness, and more. Amid ongoing student loan changes, Ascent remains committed to empowering student success and financial wellness. FAQs What alternative loan options are available if the Grad PLUS ends? If Grad PLUS loans are phased out, future graduate students should first explore financial aid that doesn’t need to be repaid such as scholarships, fellowships, grants, graduate assistantships, work-study programs, and employer tuition reimbursement programs. If there are any gaps in funding, graduate students should consider federal unsubsidized loans and private student loans. Can private student loans cover the full cost of grad school? In many cases, private student loans can cover the full cost of attending graduate school, from tuition and fees to living expenses. Private loans have unique eligibility and loan limits determined by the lender, and they usually depend on your credit history or income. That makes planning and comparing loans from different providers a necessity. Will Grad PLUS loans be forgiven? Grad PLUS loans may be eligible for forgiveness under existing federal programs like the Public Service Loan Forgiveness (PSLF) or Income-Driven Repayment (IDR) plan forgiveness, provided you meet the necessary qualifications. However, there’s no separate forgiveness initiative specifically for Grad PLUS loans at this time. -

Navigating Student Financial Aid in Changing Times: What Students and Parents Should KnowUpdate: On 3/20/25, President Donald Trump signed an executive order calling for the dismantling of the U.S. Department of Education (ED). He said during a White House event on 3/21/25 that student loans will be handled by the Small Business Administration. Read the latest news coverage here. What’s Happening with the Department of Education Every year, more than $120 billion in federal student aid moves through the U.S. Department of Education (ED) to help nearly 10 million students and their families pay for college. And while the system has had its share of administrative headaches in the past few years, it has built reliable pathways connecting students to grants, loans, and work-study jobs at thousands of schools across the nation. As you may have heard, the Trump administration is reportedly preparing an executive order that would attempt to downsize or potentially eliminate the ED, a department that manages roughly $1.7 trillion in federal student loans. This proposal is more than a policy adjustment—it would be a massive shift that could impact everything from how students apply for financial aid to the protections borrowers have. As of publication on March 13, 2025, the Trump administration initiated mass layoffs at the ED, reducing its workforce by nearly 50%. The headlines keep coming, and sifting through noise can be overwhelming when trying to grasp how it might impact your financial future. But, if you're one of the millions of students or borrowers counting on federal aid to fund your education, the truth is that these changes could directly affect your education plans and how you pay for your degree, so it’s important to stay informed. What This Could Mean For Your Education Funding If the Trump administration succeeds in dismantling the ED, what does this mean for you as a student or borrower? You've probably gotten used to filling out the Free Application for Federal Student Aid (FAFSA) a certain way, knowing who to call with questions, and understanding when your aid will arrive. With the proposed changes, financial aid could be moved to a different agency or even to state governments. And as we saw in 2024 following the troubled rollout of the FAFSA Simplification Act, changes to established processes can send ripples through the student loan ecosystem, delaying access to critical financial aid. Shift Toward Private Lenders One proposal getting a lot of attention would shift student lending from the federal government to private lenders, essentially privatizing the student loan market. If private lenders take a bigger role in financial aid, one result could be a surge of loan options for students and their families, including more flexibility in loan options and terms or specialized loans for certain majors. But there’s a trade-off. Private lenders typically have stricter credit requirements than federal programs, which means credit score and income could matter more. Given many undergraduates are just beginning to shape their career paths and may have little to no credit history or income, they may need to apply with a cosigner in order to qualify. Increase in Interest Rates & Variability If federal lending moves entirely to the private sector, borrowers might also be concerned that interest rates will increase and be more varied across different lenders and loan types. While federal loans offer the same fixed rate to everyone, private lenders adjust their rates based on a borrower’s credit profile. And, interest rates are already climbing across the board. In fact, 10-year Treasury yields (which influence all types of lending rates) have hit their highest point since 2007, which means even existing variable-rate private loans could get more expensive as the market shifts. Just like buying a house, timing matters, and the market is heating up. It will be more important than ever to choose the right private lender based not only on interest rates, but the terms and benefits they provide, such as automatic payment discounts, cash back at graduation, or access to skills training and career coaching (which we provide all borrowers through AscentUP). Fewer Paths to Loan Forgiveness For those of you already juggling federal loan repayment, you know the drill—just when you figure out the system, it changes again. The SAVE plan provides for lower monthly payments, faster paths to forgiveness, and protection from ballooning interest, but is temporarily unavailable and on shaky ground. All borrowers currently enrolled in the SAVE plan have been automatically placed into an interest-free forbearance and the time spent does not provide credit toward Public Service Loan Forgiveness (PSLF). If the SAVE plan is blocked permanently, then borrowers could face higher monthly payments, longer loan terms, and uncertainty about loan forgiveness. If you've been working toward Public Service Loan Forgiveness (PSLF), know that there is a possibility the PSLF program could be scaled back or eliminated. There is a chance that current borrowers could be grandfathered in—but you'll want to stay on top of announcements. While Ascent’s private education loans function independently from federal student loan programs, when major policy shifts occur, these changes can disrupt the entire infrastructure and potentially reshape some or all of the options available to students and their families. When a key player changes the rules of the game—all the players are impacted and have choices to make. What You Can Do We've all dealt with uncertainty before, and while it's never comfortable, you will get through it. Here are some steps you can take to help prepare for potential changes in policy: Get your paperwork in order: Organize your records of the federal aid you've received, such as award letters and loan statements, in one place. Know your numbers: Make sure you understand your current loan terms, interest rates, and repayment timeline. Knowing where your current loans stand will help you adapt if there is a change in policy. Understand how interest rates work: If there are major changes in the market, knowing how interest rates can impact your loan balance could become even more important. Here’s how to calculate your student loan interest: Find your daily interest rate (take your annual rate and divide by 365) Calculate daily interest accrual (multiply your loan balance by that daily rate) Figure monthly payments (multiply daily accrual by days in your billing cycle) Stay informed about policy changes: Follow trusted sources for updates and bookmark reliable financial aid websites like https://studentaid.gov/. Don't panic: Remember, most policy shifts roll out gradually. The changes we're discussing would likely phase in between now and October 2025, with full implementation expected by July 1, 2026. There is time to adapt and adjust your financial plans, if necessary. Explore your funding options: Understand the alternative funding options that might be available to you beyond federal student loans, including private student loans, grants, scholarships, and work-study programs. Ascent is Here to Help Whatever happens with the Department of Education, Ascent is committed to helping students and their families access and fund higher education responsibly. The landscape may change, but our priority—your educational and financial success—will not. We're in this together.

Navigating Student Financial Aid in Changing Times: What Students and Parents Should KnowUpdate: On 3/20/25, President Donald Trump signed an executive order calling for the dismantling of the U.S. Department of Education (ED). He said during a White House event on 3/21/25 that student loans will be handled by the Small Business Administration. Read the latest news coverage here. What’s Happening with the Department of Education Every year, more than $120 billion in federal student aid moves through the U.S. Department of Education (ED) to help nearly 10 million students and their families pay for college. And while the system has had its share of administrative headaches in the past few years, it has built reliable pathways connecting students to grants, loans, and work-study jobs at thousands of schools across the nation. As you may have heard, the Trump administration is reportedly preparing an executive order that would attempt to downsize or potentially eliminate the ED, a department that manages roughly $1.7 trillion in federal student loans. This proposal is more than a policy adjustment—it would be a massive shift that could impact everything from how students apply for financial aid to the protections borrowers have. As of publication on March 13, 2025, the Trump administration initiated mass layoffs at the ED, reducing its workforce by nearly 50%. The headlines keep coming, and sifting through noise can be overwhelming when trying to grasp how it might impact your financial future. But, if you're one of the millions of students or borrowers counting on federal aid to fund your education, the truth is that these changes could directly affect your education plans and how you pay for your degree, so it’s important to stay informed. What This Could Mean For Your Education Funding If the Trump administration succeeds in dismantling the ED, what does this mean for you as a student or borrower? You've probably gotten used to filling out the Free Application for Federal Student Aid (FAFSA) a certain way, knowing who to call with questions, and understanding when your aid will arrive. With the proposed changes, financial aid could be moved to a different agency or even to state governments. And as we saw in 2024 following the troubled rollout of the FAFSA Simplification Act, changes to established processes can send ripples through the student loan ecosystem, delaying access to critical financial aid. Shift Toward Private Lenders One proposal getting a lot of attention would shift student lending from the federal government to private lenders, essentially privatizing the student loan market. If private lenders take a bigger role in financial aid, one result could be a surge of loan options for students and their families, including more flexibility in loan options and terms or specialized loans for certain majors. But there’s a trade-off. Private lenders typically have stricter credit requirements than federal programs, which means credit score and income could matter more. Given many undergraduates are just beginning to shape their career paths and may have little to no credit history or income, they may need to apply with a cosigner in order to qualify. Increase in Interest Rates & Variability If federal lending moves entirely to the private sector, borrowers might also be concerned that interest rates will increase and be more varied across different lenders and loan types. While federal loans offer the same fixed rate to everyone, private lenders adjust their rates based on a borrower’s credit profile. And, interest rates are already climbing across the board. In fact, 10-year Treasury yields (which influence all types of lending rates) have hit their highest point since 2007, which means even existing variable-rate private loans could get more expensive as the market shifts. Just like buying a house, timing matters, and the market is heating up. It will be more important than ever to choose the right private lender based not only on interest rates, but the terms and benefits they provide, such as automatic payment discounts, cash back at graduation, or access to skills training and career coaching (which we provide all borrowers through AscentUP). Fewer Paths to Loan Forgiveness For those of you already juggling federal loan repayment, you know the drill—just when you figure out the system, it changes again. The SAVE plan provides for lower monthly payments, faster paths to forgiveness, and protection from ballooning interest, but is temporarily unavailable and on shaky ground. All borrowers currently enrolled in the SAVE plan have been automatically placed into an interest-free forbearance and the time spent does not provide credit toward Public Service Loan Forgiveness (PSLF). If the SAVE plan is blocked permanently, then borrowers could face higher monthly payments, longer loan terms, and uncertainty about loan forgiveness. If you've been working toward Public Service Loan Forgiveness (PSLF), know that there is a possibility the PSLF program could be scaled back or eliminated. There is a chance that current borrowers could be grandfathered in—but you'll want to stay on top of announcements. While Ascent’s private education loans function independently from federal student loan programs, when major policy shifts occur, these changes can disrupt the entire infrastructure and potentially reshape some or all of the options available to students and their families. When a key player changes the rules of the game—all the players are impacted and have choices to make. What You Can Do We've all dealt with uncertainty before, and while it's never comfortable, you will get through it. Here are some steps you can take to help prepare for potential changes in policy: Get your paperwork in order: Organize your records of the federal aid you've received, such as award letters and loan statements, in one place. Know your numbers: Make sure you understand your current loan terms, interest rates, and repayment timeline. Knowing where your current loans stand will help you adapt if there is a change in policy. Understand how interest rates work: If there are major changes in the market, knowing how interest rates can impact your loan balance could become even more important. Here’s how to calculate your student loan interest: Find your daily interest rate (take your annual rate and divide by 365) Calculate daily interest accrual (multiply your loan balance by that daily rate) Figure monthly payments (multiply daily accrual by days in your billing cycle) Stay informed about policy changes: Follow trusted sources for updates and bookmark reliable financial aid websites like https://studentaid.gov/. Don't panic: Remember, most policy shifts roll out gradually. The changes we're discussing would likely phase in between now and October 2025, with full implementation expected by July 1, 2026. There is time to adapt and adjust your financial plans, if necessary. Explore your funding options: Understand the alternative funding options that might be available to you beyond federal student loans, including private student loans, grants, scholarships, and work-study programs. Ascent is Here to Help Whatever happens with the Department of Education, Ascent is committed to helping students and their families access and fund higher education responsibly. The landscape may change, but our priority—your educational and financial success—will not. We're in this together. -

Managing Student Loan Anxiety: Tips from One Student to AnotherWhen I started college, I knew I’d be taking on student loans. However, I didn’t realize just how much it would weigh on my mind. As much as I try to focus on my classes, internship, and the overall plans for my future, the looming cloud of student debt has always been there. It’s hard to enjoy the moments of college when happiness is tied to a price tag. Over time, I’ve discovered some strategies, and small mindset shifts that have helped manage this anxiety. If you’re dealing with similar feelings, know you are not alone: according to WalletHub, 70% of students are stressed about student loans-. Loan anxiety is a shared experience for many students trying to navigate higher education. The feelings of long-term debt, worry of future job security, and fear of falling behind on payments are all common. Here are steps I’ve taken to better manage that anxiety: 1) Understand the Source For me, student loan stress comes from different sources. First, there’s the long-term commitment, knowing I’ll be making payments for years, and potentially decades, after graduation. I worry about missing payments or how one mistake can ruin things such as my credit score. Another stress I deal with is finding a job, one that can pay me enough to pay off my loans. Whether these uncertainties come from family, friends, or external pressures, they all add fuel to my anxiety. Thankfully, there are resources out there to help ease some of the stress. Ascent has great tools available to borrowers, including AscentUP, an online platform with over 50 hours of on-demand content from industry experts that supports students with financial wellness and aims to help students graduate faster, get a job that matches their needs, and earn a higher starting salary. AscentUP* helps borrowers with their academics, identifying career goals, and building confidence on how to save. It is self-paced and can be done anywhere from your mobile device. 2) Educate Yourself on Loans & Finances One of the best ways I’ve found to manage student loan anxiety is to understand exactly what I owe and how the repayment process works. Each loan type is different; whether you have taken out federal or private loans, understanding the type, term, interest rate, and repayment options will help your loans feel more manageable. For Federal Student loans, you have options: SAVE: Repayment Option: This is an income-driven repayment plan. FASFA describes it as a “plan [that] calculates your monthly payment amount based on your income and family size.” The benefits of the SAVE plan have interesting benefits. If you make your full monthly payment but fall short on paying for your monthly interest, the government will cover it! Borrowers who originally borrowed $12,000 or less receive forgiveness after 10 years. Fixed Repayment: You choose a base of monthly payments based on your income. When it comes to Fixed Repayment, there are three types. Standard Repayment Plan: A fixed monthly payment for a 10-year period. If you don’t choose a repayment plan, your loan servicer will automatically enroll you in this option. - https://studentaid.gov/manage-loans/repayment/servicers Graduated Repayment Plan: Lower payments that increase every two years, designed to be able to financially support yourself and gradually afford higher payments. Extended Repayment Plan: Offers lower fixed payments over a longer term, which is helpful for students pursuing lower-paying careers. TIP: What is Forbearance? Life can be unpredictable, especially when dealing with student loans. Forbearance is built for when life throws you curveballs and you need a temporary pause or reduction in payments. I know this seems like a lot. And each loan is different, but this is why it’s important to do research to understand your loan type. It may seem insignificant now, but loans add up and your research could potentially save hundreds, if not thousands, of dollars. The biggest takeaway is that, unlike Federal Student Loans, private student loans vary depending on the lender chosen. This is where private student loans, like Ascent, can help. Ascent offers multiple options for undergraduate loans of students to help meet their unique financial needs. For Ascent Private Student there, you also have many options: Cosigned Loans: Ideal for students with limited credit history or income. Allows students to have a credit worthy cosigner such as a parent or guardian. Non-Cosigned Loans Based on Credit: Available for students who qualify independently based on their own credit score and income. This is a great opportunity for a student to take full responsibility for their loans Non-Cosigned Outcomes Loan: This is specifically designed for juniors and seniors in college. It is an option for those that want to still support themselves ideally but might not have the facts to back it up. Instead of relying on credit scores, eligibly is determined by factors such as academic performance and projected future income. Parent Loans: This option allows parents to take out a loan on behalf of their child to help educational costs. It offers competitive rates and flexible repayment options tailored to parents. While in school, even small payments can make a big difference. Whether it’s $1, $10, or $20 a month, every contribution helps reduce the overall interest on your loan over time. Ascent allows you to make these manageable payments while still in school, giving you a head start on repayment and potentially saving you hundreds or even thousands of dollars in the long run. It's a simple way to take control of your financial future without feeling overwhelmed. I understand how easy it is to get overwhelmed when there is so much information coming to you all at once- that's exactly why I’m here to help simplify things for you. 3) Building Your Finances Starting your financial journey can be scary and intimidating. If you're not sure where to start, Ascent is here to help. With any journey you take, you have to know where to go. Trust me, as a fellow student I have been exactly where you are now. While feelings like overwhelm never disappear, there are ways to control them. Here are my personally- tested and proven tips to help during college's challenging moments. Start by creating a goal and tracking your progress. Figure out where you are financially and where you want to be to help set your goal. If you are looking for guidance with practical tips the most effective is to ask students like yourself. We have a huge list of tips for budgeting money as a college student. Once you decide what you are working towards, you can start tracking it. It will be hard to get into the habit, but forming healthy spending habits will save you in the long run. Check for student discounts and promo codes. Many popular companies, from streaming services like Hulu and Spotify to large tech companies such as Apple and Microsoft offer discounts for students. Some perks include free trial or reduced subscriptions. Most times to take advantage of these deals all you have to do is present your Student ID or sign in using your school email address. Here is a list of my favorite deals. Apply for scholarships. Take advantage of scholarships to reduce your reliance on loans. Start by researching options offered by your school, local organizations, and online. There are countless databases that will offer you aid based on your background, major, or even personal interest. Even small scholarships add up over time, and every dollar you earn through scholarships is one less dollar you must borrow. TIP: Never stop applying for scholarships!! Check out these easy no-essay scholarships from Ascent. Ascent has awarded over [scholarship_awards_amount] in scholarships to students. 4) Seeking Support and Resources Student loans can feel overwhelming, and like any kind of stress, it’s necessary to keep it all bottled up. Make sure you’re sharing your concerns and frustrations with someone you trust– whether you speak to your parents, friends, or counselor, it’s a big help to get it off your chest. And if there is no one in person you can speak to there are forums with students and professionals on College Confidential about how to deal with this anxiety. Managing student loans and the anxiety that comes with loans as it is an ongoing process; but not an impossible one. With the right tools and mindset, you can focus on moving forward with your education and future! But most critically, remind yourself that you are not alone in this journey. College is about growth and discovery, so don’t let student loans take away from what you can accomplish. College is about growth and discovery so do not let the stress of loans take away from that experience. With the right plan and support you can embrace on all the different experiences and achievements college has to offer. About the author: Maelia (Mia) Madariaga-Ilagan is a fourth-year student at University of San Diego (USD) pursuing a degree in Marketing with a minor focus in Visual Arts. Coming from a large family where all siblings are encouraged to attend college, she understands firsthand the financial pressure that student loans can bring. However, she believes that the struggle of student loans should not shadow the opportunities college brings. During her time at USD, Mia has excelled both academically and within the campus community. She has served as the Public Relations Chair for USD Associated Students and become an active member of many student organizations. These experiences and many more have shaped her growth and given her opportunities to thrive.

Managing Student Loan Anxiety: Tips from One Student to AnotherWhen I started college, I knew I’d be taking on student loans. However, I didn’t realize just how much it would weigh on my mind. As much as I try to focus on my classes, internship, and the overall plans for my future, the looming cloud of student debt has always been there. It’s hard to enjoy the moments of college when happiness is tied to a price tag. Over time, I’ve discovered some strategies, and small mindset shifts that have helped manage this anxiety. If you’re dealing with similar feelings, know you are not alone: according to WalletHub, 70% of students are stressed about student loans-. Loan anxiety is a shared experience for many students trying to navigate higher education. The feelings of long-term debt, worry of future job security, and fear of falling behind on payments are all common. Here are steps I’ve taken to better manage that anxiety: 1) Understand the Source For me, student loan stress comes from different sources. First, there’s the long-term commitment, knowing I’ll be making payments for years, and potentially decades, after graduation. I worry about missing payments or how one mistake can ruin things such as my credit score. Another stress I deal with is finding a job, one that can pay me enough to pay off my loans. Whether these uncertainties come from family, friends, or external pressures, they all add fuel to my anxiety. Thankfully, there are resources out there to help ease some of the stress. Ascent has great tools available to borrowers, including AscentUP, an online platform with over 50 hours of on-demand content from industry experts that supports students with financial wellness and aims to help students graduate faster, get a job that matches their needs, and earn a higher starting salary. AscentUP* helps borrowers with their academics, identifying career goals, and building confidence on how to save. It is self-paced and can be done anywhere from your mobile device. 2) Educate Yourself on Loans & Finances One of the best ways I’ve found to manage student loan anxiety is to understand exactly what I owe and how the repayment process works. Each loan type is different; whether you have taken out federal or private loans, understanding the type, term, interest rate, and repayment options will help your loans feel more manageable. For Federal Student loans, you have options: SAVE: Repayment Option: This is an income-driven repayment plan. FASFA describes it as a “plan [that] calculates your monthly payment amount based on your income and family size.” The benefits of the SAVE plan have interesting benefits. If you make your full monthly payment but fall short on paying for your monthly interest, the government will cover it! Borrowers who originally borrowed $12,000 or less receive forgiveness after 10 years. Fixed Repayment: You choose a base of monthly payments based on your income. When it comes to Fixed Repayment, there are three types. Standard Repayment Plan: A fixed monthly payment for a 10-year period. If you don’t choose a repayment plan, your loan servicer will automatically enroll you in this option. - https://studentaid.gov/manage-loans/repayment/servicers Graduated Repayment Plan: Lower payments that increase every two years, designed to be able to financially support yourself and gradually afford higher payments. Extended Repayment Plan: Offers lower fixed payments over a longer term, which is helpful for students pursuing lower-paying careers. TIP: What is Forbearance? Life can be unpredictable, especially when dealing with student loans. Forbearance is built for when life throws you curveballs and you need a temporary pause or reduction in payments. I know this seems like a lot. And each loan is different, but this is why it’s important to do research to understand your loan type. It may seem insignificant now, but loans add up and your research could potentially save hundreds, if not thousands, of dollars. The biggest takeaway is that, unlike Federal Student Loans, private student loans vary depending on the lender chosen. This is where private student loans, like Ascent, can help. Ascent offers multiple options for undergraduate loans of students to help meet their unique financial needs. For Ascent Private Student there, you also have many options: Cosigned Loans: Ideal for students with limited credit history or income. Allows students to have a credit worthy cosigner such as a parent or guardian. Non-Cosigned Loans Based on Credit: Available for students who qualify independently based on their own credit score and income. This is a great opportunity for a student to take full responsibility for their loans Non-Cosigned Outcomes Loan: This is specifically designed for juniors and seniors in college. It is an option for those that want to still support themselves ideally but might not have the facts to back it up. Instead of relying on credit scores, eligibly is determined by factors such as academic performance and projected future income. Parent Loans: This option allows parents to take out a loan on behalf of their child to help educational costs. It offers competitive rates and flexible repayment options tailored to parents. While in school, even small payments can make a big difference. Whether it’s $1, $10, or $20 a month, every contribution helps reduce the overall interest on your loan over time. Ascent allows you to make these manageable payments while still in school, giving you a head start on repayment and potentially saving you hundreds or even thousands of dollars in the long run. It's a simple way to take control of your financial future without feeling overwhelmed. I understand how easy it is to get overwhelmed when there is so much information coming to you all at once- that's exactly why I’m here to help simplify things for you. 3) Building Your Finances Starting your financial journey can be scary and intimidating. If you're not sure where to start, Ascent is here to help. With any journey you take, you have to know where to go. Trust me, as a fellow student I have been exactly where you are now. While feelings like overwhelm never disappear, there are ways to control them. Here are my personally- tested and proven tips to help during college's challenging moments. Start by creating a goal and tracking your progress. Figure out where you are financially and where you want to be to help set your goal. If you are looking for guidance with practical tips the most effective is to ask students like yourself. We have a huge list of tips for budgeting money as a college student. Once you decide what you are working towards, you can start tracking it. It will be hard to get into the habit, but forming healthy spending habits will save you in the long run. Check for student discounts and promo codes. Many popular companies, from streaming services like Hulu and Spotify to large tech companies such as Apple and Microsoft offer discounts for students. Some perks include free trial or reduced subscriptions. Most times to take advantage of these deals all you have to do is present your Student ID or sign in using your school email address. Here is a list of my favorite deals. Apply for scholarships. Take advantage of scholarships to reduce your reliance on loans. Start by researching options offered by your school, local organizations, and online. There are countless databases that will offer you aid based on your background, major, or even personal interest. Even small scholarships add up over time, and every dollar you earn through scholarships is one less dollar you must borrow. TIP: Never stop applying for scholarships!! Check out these easy no-essay scholarships from Ascent. Ascent has awarded over [scholarship_awards_amount] in scholarships to students. 4) Seeking Support and Resources Student loans can feel overwhelming, and like any kind of stress, it’s necessary to keep it all bottled up. Make sure you’re sharing your concerns and frustrations with someone you trust– whether you speak to your parents, friends, or counselor, it’s a big help to get it off your chest. And if there is no one in person you can speak to there are forums with students and professionals on College Confidential about how to deal with this anxiety. Managing student loans and the anxiety that comes with loans as it is an ongoing process; but not an impossible one. With the right tools and mindset, you can focus on moving forward with your education and future! But most critically, remind yourself that you are not alone in this journey. College is about growth and discovery, so don’t let student loans take away from what you can accomplish. College is about growth and discovery so do not let the stress of loans take away from that experience. With the right plan and support you can embrace on all the different experiences and achievements college has to offer. About the author: Maelia (Mia) Madariaga-Ilagan is a fourth-year student at University of San Diego (USD) pursuing a degree in Marketing with a minor focus in Visual Arts. Coming from a large family where all siblings are encouraged to attend college, she understands firsthand the financial pressure that student loans can bring. However, she believes that the struggle of student loans should not shadow the opportunities college brings. During her time at USD, Mia has excelled both academically and within the campus community. She has served as the Public Relations Chair for USD Associated Students and become an active member of many student organizations. These experiences and many more have shaped her growth and given her opportunities to thrive. -

FAFSA Eligibility: Who Qualifies and Income LimitsWondering if you qualify for federal financial aid? Learn more about the eligibility requirements while submitting your Free Application for Federal Student Aid (FAFSA).

FAFSA Eligibility: Who Qualifies and Income LimitsWondering if you qualify for federal financial aid? Learn more about the eligibility requirements while submitting your Free Application for Federal Student Aid (FAFSA). -