-

Ascent Named Best Places to Work in Fintech 2026Ascent, a leading provider of innovative financial products and student support services that enable more students to access education and achieve academic and economic success, has been named one of the 2026 Best Places to Work in Fintech, an awards program created in 2017 by Arizent and Best Companies Group. This annual survey and awards program recognizes the top employers in the financial technology industry. Honorees operate across a wide range of financial services sectors, including banking, mortgages, insurance, payments and financial advisory. To be eligible, companies must provide technology products or services that support financial services delivery, have been in business for at least one year, and employ at least 15 people in the U.S. "Each year, the Best Places to Work in Financial Technology offers a glimpse into the practices of fintechs whose employees rate their workplaces highly," said Penny Crosman, executive editor of technology at American Banker. "This year, employees appear to value remote work and schedule flexibility above all else, at a time when many traditional financial firms have enforced strict return-to-work policies." Companies from across the United States entered a two-part survey process to determine Arizent’s Best Places to Work in Fintech. The first part consisted of evaluating each nominated company's workplace policies, practices, philosophy, systems and demographics. The second part consisted of an employee survey to measure the employee experience. The combined scores determined the top companies and the final ranking. Best Companies Group managed the overall registration and survey process, analyzed the data and determined the final ranking. “We’re proud to have built a workplace where employees feel trusted, supported, and genuinely connected to the work they do,” said Emily Skoubo, Director of Human Resources at Ascent. “This recognition reflects the collaborative culture our team has created together and our continued focus on providing an environment where people can grow, contribute, and feel valued.” For more information on Arizent’s Best Places to Work in Fintech program, including full eligibility criteria, visit www.BestPlacestoWorkFinTech.com or contact Penny Crosman at [email protected]. About Ascent Ascent is a leading provider of innovative financial products and wrap-around student support services that enable more students to access education and achieve academic and economic success. Everything Ascent offers is designed by leading industry professionals and with advanced technology and innovation to increase every student’s ability to plan, pay, and succeed. Ascent’s rare Outcomes-based Loan provides funding to credit-invisible borrowers who generally do not benefit from traditional credit. Ascent products also include: Cosigned Loans, Solo Loans, Career Loans, Parent Loans, Graduate Loans, Access Loans, Enterprise Loans and Impact Loans.

Ascent Named Best Places to Work in Fintech 2026Ascent, a leading provider of innovative financial products and student support services that enable more students to access education and achieve academic and economic success, has been named one of the 2026 Best Places to Work in Fintech, an awards program created in 2017 by Arizent and Best Companies Group. This annual survey and awards program recognizes the top employers in the financial technology industry. Honorees operate across a wide range of financial services sectors, including banking, mortgages, insurance, payments and financial advisory. To be eligible, companies must provide technology products or services that support financial services delivery, have been in business for at least one year, and employ at least 15 people in the U.S. "Each year, the Best Places to Work in Financial Technology offers a glimpse into the practices of fintechs whose employees rate their workplaces highly," said Penny Crosman, executive editor of technology at American Banker. "This year, employees appear to value remote work and schedule flexibility above all else, at a time when many traditional financial firms have enforced strict return-to-work policies." Companies from across the United States entered a two-part survey process to determine Arizent’s Best Places to Work in Fintech. The first part consisted of evaluating each nominated company's workplace policies, practices, philosophy, systems and demographics. The second part consisted of an employee survey to measure the employee experience. The combined scores determined the top companies and the final ranking. Best Companies Group managed the overall registration and survey process, analyzed the data and determined the final ranking. “We’re proud to have built a workplace where employees feel trusted, supported, and genuinely connected to the work they do,” said Emily Skoubo, Director of Human Resources at Ascent. “This recognition reflects the collaborative culture our team has created together and our continued focus on providing an environment where people can grow, contribute, and feel valued.” For more information on Arizent’s Best Places to Work in Fintech program, including full eligibility criteria, visit www.BestPlacestoWorkFinTech.com or contact Penny Crosman at [email protected]. About Ascent Ascent is a leading provider of innovative financial products and wrap-around student support services that enable more students to access education and achieve academic and economic success. Everything Ascent offers is designed by leading industry professionals and with advanced technology and innovation to increase every student’s ability to plan, pay, and succeed. Ascent’s rare Outcomes-based Loan provides funding to credit-invisible borrowers who generally do not benefit from traditional credit. Ascent products also include: Cosigned Loans, Solo Loans, Career Loans, Parent Loans, Graduate Loans, Access Loans, Enterprise Loans and Impact Loans. -

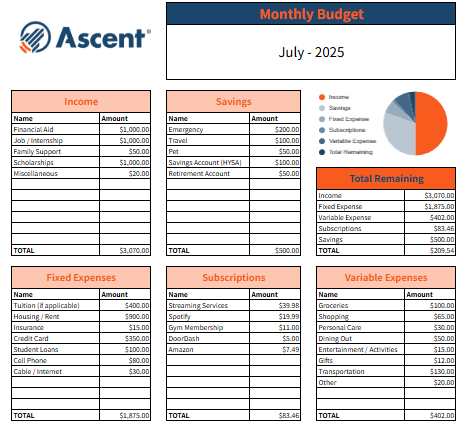

Smart Money Moves: The Ultimate Guide to Budgeting for College StudentsCollege is an exciting time to explore, grow, and gain independence—including getting comfortable with money. Budgeting might sound intimidating, but it’s really just a way to make sure your money supports the life you want to live. With the right strategy and tools, any student can manage money effectively, reduce stress, and set themselves up for future financial success. Why Budgeting is Crucial for College Students Budgeting gives you control over your money, even when it feels like you don’t have much. It helps you cover essentials, avoid debt, and still enjoy life on and off campus. Whether you’re managing a part-time income or student loans, a budget keeps you organized, prepared for surprises, and builds good habits for life after college. Step 1: Understand Your Finances – Creating a Realistic Budget Before you can build a budget that works, you need to understand where your money is coming from and where it’s going. Taking the time to get clear on your income, expenses, and savings goals is the foundation of smart money management. Track Your Income Sources: Before you can plan how to spend or save, it’s important to know how much money you have coming in. Identifying all your income sources will give you a clear starting point for your budget. Financial aid (grants, scholarships, loans) Job income Family support or allowance Know Your Expenses: Prioritize Needs vs. Wants Once you understand your income, the next step is to track your spending. Breaking your expenses into needs and wants can help you make smarter decisions about where your money goes. Fixed Expenses (Needs): Tuition, rent, utilities, insurance, credit cards, bills Variable Expenses (Wants): Food, entertainment, supplies, clothing, personal care Savings: Fund Your Future Saving might not feel urgent right now, but it’s one of the most powerful habits you can start. Even small contributions help you build a financial safety net and encourage long-term habits that will support your goals well beyond college. Savings Accounts: Emergency Fund, travel expenses, pet care High Yield Savings Account: Have higher interest rates and enable faster growth of your savings Retirement Plans (401k, Roth IRA): Tax-advantaged savings plans to help grow savings over time for retirement expenses Use a Budgeting Method Choosing a budgeting method gives structure to your financial plan and helps you stay consistent with your spending, savings, and goals. 50/30/20 Rule: 50% needs, 30% wants, 20% savings/debt repayment This rule helps individuals manage their finances by prioritizing essential expenses, discretionary spending, and long-term financial goals. 50% Needs: Essential expenses you must pay to live and work 30% Wants: Non-essential but enhance quality of life 20% Savings: Strengthening your financial future Envelope Method: Physical or digital envelopes for each category Determine budget categories Set monthly budget for each Withdraw cash and fill envelopes Spend only from those envelopes Step 2: Save Where You Can Once you’ve built a basic budget, the next step is finding ways to stretch your dollars further. The good news? As a college student, there are tons of easy ways to save without sacrificing fun or convenience. From student discounts to smart spending habits, a few small changes can make a big difference. Here’s how to make the most of what you have. Student discounts: Show student ID at restaurants, shopping stores, movie theaters, etc. Apps to get student discounts: UNiDAYS, Student Beans Textbooks: Rent, buy used, library copies Food: Cook at home, use meal plans wisely, avoid daily coffee shop habits, check supermarket ads for deals Transportation: Use public transit, bike, or carpool Most colleges provide free transportation passes Entertainment: Attend free campus events, share streaming accounts Step 3: Prepare for the Unexpected Even the best budgets can be thrown off by surprise expenses. Whether it’s a last-minute trip home, a medical bill, or an extra textbook you didn’t plan for, life happens. That’s why it’s important to build a financial cushion that helps you handle the unexpected without stress—or debt. Here’s how to stay prepared and protect your budget. Build an Emergency Fund: Aim for a $500 goal to start Plan for Irregular Expenses: Books, holidays, trips, birthdays, medical expenses Step 4: Use Tools to Stay on Track Creating a budget is a great start—but staying on track takes a little help. Thankfully, there are plenty of simple tools that can keep you organized and consistent, even on your busiest days. Whether you prefer apps, spreadsheets, or calendar reminders, the right tools can make managing your money quicker, easier, and less stressful. Let’s look at a few that can help you stay in control. Spreadsheets: Custom Google Sheets or Excel Download Ascent’s Student Budgeting Sheet here! Banking Tools: Auto alerts for low balance, spending summaries Calendar Reminders: For bill due dates and budget check-ins Block specific date/time on your calendar to sort your finances Common Budgeting Mistakes to Avoid Even with the best intentions, it’s easy to slip up. Being aware of common budgeting mistakes can help you stay on track and avoid unnecessary stress. Here are a few pitfalls to watch out for: Underestimating daily spending: Every purchase adds up! Not reviewing your budget monthly: Adjust for changes Overlooking one-time costs: Move-in costs, graduation fees, etc. Relying on your credit cards: Make sure you have the funds to pay them back Building Healthy Financial Habits Good budgeting isn’t just about numbers—it’s about building habits that support your goals over time. With a few consistent practices, managing your money can become second nature. Here’s how to turn smart choices into lasting habits: Track every dollar: Even small purchases add up Set time aside time to review your account weekly Set your goals: avoid overdrafts, reduce credit card use Stick to your budget for 3 months? Treat yourself (responsibly)! Final Thoughts Budgeting is an essential skill that can make your college experience less stressful and more empowering. It’s not about getting everything right the first time—it’s about starting small, staying flexible, and learning from your experiences. With a little effort and consistency, you’ll build habits that not only help you thrive in college but also set you up for long-term financial success.

Smart Money Moves: The Ultimate Guide to Budgeting for College StudentsCollege is an exciting time to explore, grow, and gain independence—including getting comfortable with money. Budgeting might sound intimidating, but it’s really just a way to make sure your money supports the life you want to live. With the right strategy and tools, any student can manage money effectively, reduce stress, and set themselves up for future financial success. Why Budgeting is Crucial for College Students Budgeting gives you control over your money, even when it feels like you don’t have much. It helps you cover essentials, avoid debt, and still enjoy life on and off campus. Whether you’re managing a part-time income or student loans, a budget keeps you organized, prepared for surprises, and builds good habits for life after college. Step 1: Understand Your Finances – Creating a Realistic Budget Before you can build a budget that works, you need to understand where your money is coming from and where it’s going. Taking the time to get clear on your income, expenses, and savings goals is the foundation of smart money management. Track Your Income Sources: Before you can plan how to spend or save, it’s important to know how much money you have coming in. Identifying all your income sources will give you a clear starting point for your budget. Financial aid (grants, scholarships, loans) Job income Family support or allowance Know Your Expenses: Prioritize Needs vs. Wants Once you understand your income, the next step is to track your spending. Breaking your expenses into needs and wants can help you make smarter decisions about where your money goes. Fixed Expenses (Needs): Tuition, rent, utilities, insurance, credit cards, bills Variable Expenses (Wants): Food, entertainment, supplies, clothing, personal care Savings: Fund Your Future Saving might not feel urgent right now, but it’s one of the most powerful habits you can start. Even small contributions help you build a financial safety net and encourage long-term habits that will support your goals well beyond college. Savings Accounts: Emergency Fund, travel expenses, pet care High Yield Savings Account: Have higher interest rates and enable faster growth of your savings Retirement Plans (401k, Roth IRA): Tax-advantaged savings plans to help grow savings over time for retirement expenses Use a Budgeting Method Choosing a budgeting method gives structure to your financial plan and helps you stay consistent with your spending, savings, and goals. 50/30/20 Rule: 50% needs, 30% wants, 20% savings/debt repayment This rule helps individuals manage their finances by prioritizing essential expenses, discretionary spending, and long-term financial goals. 50% Needs: Essential expenses you must pay to live and work 30% Wants: Non-essential but enhance quality of life 20% Savings: Strengthening your financial future Envelope Method: Physical or digital envelopes for each category Determine budget categories Set monthly budget for each Withdraw cash and fill envelopes Spend only from those envelopes Step 2: Save Where You Can Once you’ve built a basic budget, the next step is finding ways to stretch your dollars further. The good news? As a college student, there are tons of easy ways to save without sacrificing fun or convenience. From student discounts to smart spending habits, a few small changes can make a big difference. Here’s how to make the most of what you have. Student discounts: Show student ID at restaurants, shopping stores, movie theaters, etc. Apps to get student discounts: UNiDAYS, Student Beans Textbooks: Rent, buy used, library copies Food: Cook at home, use meal plans wisely, avoid daily coffee shop habits, check supermarket ads for deals Transportation: Use public transit, bike, or carpool Most colleges provide free transportation passes Entertainment: Attend free campus events, share streaming accounts Step 3: Prepare for the Unexpected Even the best budgets can be thrown off by surprise expenses. Whether it’s a last-minute trip home, a medical bill, or an extra textbook you didn’t plan for, life happens. That’s why it’s important to build a financial cushion that helps you handle the unexpected without stress—or debt. Here’s how to stay prepared and protect your budget. Build an Emergency Fund: Aim for a $500 goal to start Plan for Irregular Expenses: Books, holidays, trips, birthdays, medical expenses Step 4: Use Tools to Stay on Track Creating a budget is a great start—but staying on track takes a little help. Thankfully, there are plenty of simple tools that can keep you organized and consistent, even on your busiest days. Whether you prefer apps, spreadsheets, or calendar reminders, the right tools can make managing your money quicker, easier, and less stressful. Let’s look at a few that can help you stay in control. Spreadsheets: Custom Google Sheets or Excel Download Ascent’s Student Budgeting Sheet here! Banking Tools: Auto alerts for low balance, spending summaries Calendar Reminders: For bill due dates and budget check-ins Block specific date/time on your calendar to sort your finances Common Budgeting Mistakes to Avoid Even with the best intentions, it’s easy to slip up. Being aware of common budgeting mistakes can help you stay on track and avoid unnecessary stress. Here are a few pitfalls to watch out for: Underestimating daily spending: Every purchase adds up! Not reviewing your budget monthly: Adjust for changes Overlooking one-time costs: Move-in costs, graduation fees, etc. Relying on your credit cards: Make sure you have the funds to pay them back Building Healthy Financial Habits Good budgeting isn’t just about numbers—it’s about building habits that support your goals over time. With a few consistent practices, managing your money can become second nature. Here’s how to turn smart choices into lasting habits: Track every dollar: Even small purchases add up Set time aside time to review your account weekly Set your goals: avoid overdrafts, reduce credit card use Stick to your budget for 3 months? Treat yourself (responsibly)! Final Thoughts Budgeting is an essential skill that can make your college experience less stressful and more empowering. It’s not about getting everything right the first time—it’s about starting small, staying flexible, and learning from your experiences. With a little effort and consistency, you’ll build habits that not only help you thrive in college but also set you up for long-term financial success. -

A Student’s Guide to Smart Summer Spending & SavingIt’s finally summer! Whether you're kicking off your mornings with a run, gaming with friends, or soaking up the sun poolside, this is your time to unwind. While the season is all about fun and freedom, it’s also a great opportunity to be mindful of your money. The choices you make now—both in spending and saving—can set you up for a smoother, more stress-free school year. Save this Summer Open a Savings Account Even small deposits from a paycheck or birthday card can add up fast. Credit unions often offer student-friendly savings accounts that help you set goals, earn interest, and build smart financial habits. You can even automate your deposits—just set it and forget it! SAFE Credit Union has some great savings account options—from traditional savings to high-dividend savings accounts—so you can start your savings journey now. Apply for Scholarships Applying for scholarships is a wonderful way to save money this summer! Ascent Funding offers a $1,000 scholarship giveaway every month; no essay required! Budget Around Plans but Leave Room for Spontaneity Create a simple monthly budget based on your known expenses—like back-to-school shopping, beach days, or a friend’s birthday. Then, add a “spontaneous spending” cap. Whether it’s $30 or $100, this lets you enjoy last-minute BBQs or froyo runs without wondering where your money went. Use SAFE Credit Union’s financial guides or your favorite app to stay on track. Apply the 24-Hour Rule Thinking about that $65 pair of sunglasses or a $90 concert outfit? Wait 24 hours. Still want it tomorrow? Go for it. For bigger purchases, wait 48–72 hours. It gives you time to check your budget and see if it’s really worth it. Use Student Discounts Student status = Savings. Apps like UNiDAYS and Student Beans offer deals on clothes, tech, food, and gym memberships. Always ask: “Do you offer student discounts?” You’d be surprised how often the answer is yes! Try a No-Spend Challenge Pick a weekend—or even just a day— where you only spend on necessities. It’s a fun, low-pressure way to reset your habits, be more intentional, and boost savings. Go on a Staycation You don’t need a passport to have fun. Explore your city like a tourist—check out local concerts, free museum days, night markets, or hiking trails. You’ll save hundreds on travel while still making memories. Smart Summer Splurges Invest in Timeless Summer Staples Choose breathable, durable fabrics like cotton and linen. Stick to neutral colors and classic styles that won’t go out of fashion. Think cost-per-wear for long-term savings. Prioritize Health: Buy the Sunscreen Sunscreen isn’t optional—it’s both self-care and long-term financial protection. A $10 bottle now is less than future medical costs. Pro tip: Buy in bulk or check for student discounts at local stores. Final Thoughts There are infinite ways to spend and save responsibly. It’s an easy way to stay in control of your money this summer, and come fall, you’ll be glad you did! About the Author Kristina Nguyen is a community college student studying Business Administration with an emphasis in Marketing. As President of the Business Club and Transfer Club at her school, she helps students navigate the transfer process, connect with industry professionals, and access scholarship resources. After graduating from high school at 16, Kristina entered community college unsure of what to expect and unaware of the many opportunities available. Now, as she prepares for her own transfer to a four-year university, she’s passionate about helping other students feel confident in their journey and realizes there’s no shame in taking an alternative route to their goals.

A Student’s Guide to Smart Summer Spending & SavingIt’s finally summer! Whether you're kicking off your mornings with a run, gaming with friends, or soaking up the sun poolside, this is your time to unwind. While the season is all about fun and freedom, it’s also a great opportunity to be mindful of your money. The choices you make now—both in spending and saving—can set you up for a smoother, more stress-free school year. Save this Summer Open a Savings Account Even small deposits from a paycheck or birthday card can add up fast. Credit unions often offer student-friendly savings accounts that help you set goals, earn interest, and build smart financial habits. You can even automate your deposits—just set it and forget it! SAFE Credit Union has some great savings account options—from traditional savings to high-dividend savings accounts—so you can start your savings journey now. Apply for Scholarships Applying for scholarships is a wonderful way to save money this summer! Ascent Funding offers a $1,000 scholarship giveaway every month; no essay required! Budget Around Plans but Leave Room for Spontaneity Create a simple monthly budget based on your known expenses—like back-to-school shopping, beach days, or a friend’s birthday. Then, add a “spontaneous spending” cap. Whether it’s $30 or $100, this lets you enjoy last-minute BBQs or froyo runs without wondering where your money went. Use SAFE Credit Union’s financial guides or your favorite app to stay on track. Apply the 24-Hour Rule Thinking about that $65 pair of sunglasses or a $90 concert outfit? Wait 24 hours. Still want it tomorrow? Go for it. For bigger purchases, wait 48–72 hours. It gives you time to check your budget and see if it’s really worth it. Use Student Discounts Student status = Savings. Apps like UNiDAYS and Student Beans offer deals on clothes, tech, food, and gym memberships. Always ask: “Do you offer student discounts?” You’d be surprised how often the answer is yes! Try a No-Spend Challenge Pick a weekend—or even just a day— where you only spend on necessities. It’s a fun, low-pressure way to reset your habits, be more intentional, and boost savings. Go on a Staycation You don’t need a passport to have fun. Explore your city like a tourist—check out local concerts, free museum days, night markets, or hiking trails. You’ll save hundreds on travel while still making memories. Smart Summer Splurges Invest in Timeless Summer Staples Choose breathable, durable fabrics like cotton and linen. Stick to neutral colors and classic styles that won’t go out of fashion. Think cost-per-wear for long-term savings. Prioritize Health: Buy the Sunscreen Sunscreen isn’t optional—it’s both self-care and long-term financial protection. A $10 bottle now is less than future medical costs. Pro tip: Buy in bulk or check for student discounts at local stores. Final Thoughts There are infinite ways to spend and save responsibly. It’s an easy way to stay in control of your money this summer, and come fall, you’ll be glad you did! About the Author Kristina Nguyen is a community college student studying Business Administration with an emphasis in Marketing. As President of the Business Club and Transfer Club at her school, she helps students navigate the transfer process, connect with industry professionals, and access scholarship resources. After graduating from high school at 16, Kristina entered community college unsure of what to expect and unaware of the many opportunities available. Now, as she prepares for her own transfer to a four-year university, she’s passionate about helping other students feel confident in their journey and realizes there’s no shame in taking an alternative route to their goals. -

How Graduate Students Can Adjust to Grad Plus Loan NewsStudent loans are a hot topic these days, and for good reason. There have been massive shake ups in education under the Trump administration, from the proposed dissolution of the U.S. Department of Education to sweeping changes to how student loans could be administered and managed in the future. The potential impact of these proposed changes is not limited to undergrads and future college students and their families. With the cost of a master's degree averaging between $44,000 to $71,000, many graduate students also rely on federal student aid, such as Grad PLUS loans, to fund their continuing education. If you’re a grad student, you're probably wondering how these changes might impact your future and your ability to pay for graduate school. Let's walk through the potential changes and explore some alternative financial aid options, should Grad PLUS loans become unavailable. Key Takeaways Grad PLUS loans are a type of federal loan offered by the U.S. Department of Education that can cover up to the full cost of attending graduate school. Republican lawmakers have proposed changes to the federal student loan programs that administer graduate loans, including reduced caps on unsubsidized loans and eliminating Grad PLUS loans altogether. If these proposed changes become law, current graduate students will likely be grandfathered in, but future graduate students may need to seek alternative sources of financial aid. Scholarships, fellowships, need-based grants, graduate assistantships, work-study programs, federal unsubsidized loans, and private student loans are alternative funding options graduate students can consider. What Are Grad PLUS Loans? Grad PLUS loans are a type of Direct PLUS loan specifically for eligible graduate and professional students. These credit-based federal loans are offered by the U.S. Department of Education and allow students to borrow up to the full cost of attendance (graduate tuition, fees, and living expenses) minus any other financial aid received. They come with a fixed interest rate and borrower protections, and they’re a popular option because federal unsubsidized loans often don’t cover the full cost of advanced degrees. According to recent federal data, Grad PLUS loans account for a significant portion of graduate student debt. As many as 1.8 million borrowers hold these loans, totaling up to $117.2 billion. This has caught the attention of some policymakers, who are starting to take a closer look at these loans. The high borrowing limits and growing debt load have sparked increased scrutiny of Grad PLUS loans, especially as discussions around the student loan crisis and reforms have intensified. Policymakers are raising the possibility of reform—or even elimination—as ways to reduce the overall burden of graduate-level debt. Will the Grad PLUS Loan Program be Cut? Discussions around eliminating the Grad PLUS loan program have gained traction on Capitol Hill, especially among Republican lawmakers who want to rein in federal spending on graduate education. These lawmakers argue that unlimited borrowing under the program inflates the cost of graduate degrees and places an undue debt burden on students. They’ve introduced bills such as the College Cost Reduction Act of 2024, which proposed eliminating Direct PLUS loans. While it didn’t pass, similar themes in legislation have been introduced in 2025. The Graduate Opportunity and Affordable Loans Act, introduced by Alabama Senator Tommy Tuberville in January 2025, proposes to eliminate the ability of graduate and professional students to receive Direct PLUS loans and sets the aggregate limit on unsubsidized loans to $65,000 for a graduate student. While the bill was referred to the Committee on Health, Education, Labor, and Pensions, it has yet to proceed. Even though neither bill targeting Grad PLUS loans has passed, they each signal lawmakers’ appetite for reforming graduate lending. That means potential changes to how students finance advanced degrees. What Grad PLUS Loan News Means for Borrowers As policymakers debate the future of federal student aid, Grad PLUS loans are undeniably on the chopping block. For current and prospective graduate students, that adds another layer of uncertainty to an already stressful financial climate. Rising tuition costs and fewer affordable borrowing options could leave many students scrambling to cover expenses. Finding student loans for graduate school, including from private lenders, will become more necessary for students who’ve exhausted free financial aid options. Current Grad PLUS Borrowers Students already enrolled or recent graduates with active Grad PLUS loans probably won’t see major changes, at least in the short term. If Congress eliminates the program, existing borrowers will likely be “grandfathered” in, meaning they can keep their current loans and repayment terms as they are. The uncertainty around the Grad PLUS loan 2024-2025 cycle could complicate financial planning for those midway through multi-year programs. If you’re in either of these groups, pay close attention to Grad PLUS loan news developments and start researching backup funding strategies in case future borrowing under Grad PLUS is capped or phased out. Future Grad PLUS Borrowers Future graduate students might be at bigger risk of losing out on Grad PLUS funding. If this federal loan program is eliminated, students may need to rely more heavily on private loans to finance their education. While private loans are just as effective at funding advanced degrees and may offer additional benefits like access to career readiness tools, they may also come with tighter credit requirements, variable interest rates, and other considerations—so it is important to compare your options. This shift from federal to private loans could disproportionately impact students with limited or poor credit histories. As a result, some may delay graduate studies, choose lower-cost institutions, or seek employer-sponsored education benefits. Others may turn to part-time enrollment or work full-time when studying, lengthening the time needed to complete a degree. If you’re thinking about attending grad school, now is the time to start preparing: Compare graduate program costs and consider how you might pay for your desired program if Grad PLUS loans go away. Research and apply for graduate scholarships, fellowships, and other grants. To do so, you’ll need to complete the Free Application for Federal Student Aid (FAFSA) every year. Apply for graduate assistantships or federal work-study programs. Availability of these programs may impact your school choice. Look into employer education benefits to help cover the cost of graduate school. Take steps to build a strong credit profile, research private loan terms, and prepare to borrow if you still need to cover costs. Ascent Is Here to Help We know that paying for grad school is an important concern for all students, and that Grad PLUS loans have been a vital resource. Even if they go away, however, there are still options. Try to be selective about your desired program, pursue all your options for free financial aid, and take your time comparing lenders for private student loans. Ascent can help you find the right loan terms and interest rate to support your graduate education, but we’re here for you beyond borrowing. Our resources for students and families offer guidance about paying for school, better budgeting, career-readiness, and more. Amid ongoing student loan changes, Ascent remains committed to empowering student success and financial wellness. FAQs What alternative loan options are available if the Grad PLUS ends? If Grad PLUS loans are phased out, future graduate students should first explore financial aid that doesn’t need to be repaid such as scholarships, fellowships, grants, graduate assistantships, work-study programs, and employer tuition reimbursement programs. If there are any gaps in funding, graduate students should consider federal unsubsidized loans and private student loans. Can private student loans cover the full cost of grad school? In many cases, private student loans can cover the full cost of attending graduate school, from tuition and fees to living expenses. Private loans have unique eligibility and loan limits determined by the lender, and they usually depend on your credit history or income. That makes planning and comparing loans from different providers a necessity. Will Grad PLUS loans be forgiven? Grad PLUS loans may be eligible for forgiveness under existing federal programs like the Public Service Loan Forgiveness (PSLF) or Income-Driven Repayment (IDR) plan forgiveness, provided you meet the necessary qualifications. However, there’s no separate forgiveness initiative specifically for Grad PLUS loans at this time.

How Graduate Students Can Adjust to Grad Plus Loan NewsStudent loans are a hot topic these days, and for good reason. There have been massive shake ups in education under the Trump administration, from the proposed dissolution of the U.S. Department of Education to sweeping changes to how student loans could be administered and managed in the future. The potential impact of these proposed changes is not limited to undergrads and future college students and their families. With the cost of a master's degree averaging between $44,000 to $71,000, many graduate students also rely on federal student aid, such as Grad PLUS loans, to fund their continuing education. If you’re a grad student, you're probably wondering how these changes might impact your future and your ability to pay for graduate school. Let's walk through the potential changes and explore some alternative financial aid options, should Grad PLUS loans become unavailable. Key Takeaways Grad PLUS loans are a type of federal loan offered by the U.S. Department of Education that can cover up to the full cost of attending graduate school. Republican lawmakers have proposed changes to the federal student loan programs that administer graduate loans, including reduced caps on unsubsidized loans and eliminating Grad PLUS loans altogether. If these proposed changes become law, current graduate students will likely be grandfathered in, but future graduate students may need to seek alternative sources of financial aid. Scholarships, fellowships, need-based grants, graduate assistantships, work-study programs, federal unsubsidized loans, and private student loans are alternative funding options graduate students can consider. What Are Grad PLUS Loans? Grad PLUS loans are a type of Direct PLUS loan specifically for eligible graduate and professional students. These credit-based federal loans are offered by the U.S. Department of Education and allow students to borrow up to the full cost of attendance (graduate tuition, fees, and living expenses) minus any other financial aid received. They come with a fixed interest rate and borrower protections, and they’re a popular option because federal unsubsidized loans often don’t cover the full cost of advanced degrees. According to recent federal data, Grad PLUS loans account for a significant portion of graduate student debt. As many as 1.8 million borrowers hold these loans, totaling up to $117.2 billion. This has caught the attention of some policymakers, who are starting to take a closer look at these loans. The high borrowing limits and growing debt load have sparked increased scrutiny of Grad PLUS loans, especially as discussions around the student loan crisis and reforms have intensified. Policymakers are raising the possibility of reform—or even elimination—as ways to reduce the overall burden of graduate-level debt. Will the Grad PLUS Loan Program be Cut? Discussions around eliminating the Grad PLUS loan program have gained traction on Capitol Hill, especially among Republican lawmakers who want to rein in federal spending on graduate education. These lawmakers argue that unlimited borrowing under the program inflates the cost of graduate degrees and places an undue debt burden on students. They’ve introduced bills such as the College Cost Reduction Act of 2024, which proposed eliminating Direct PLUS loans. While it didn’t pass, similar themes in legislation have been introduced in 2025. The Graduate Opportunity and Affordable Loans Act, introduced by Alabama Senator Tommy Tuberville in January 2025, proposes to eliminate the ability of graduate and professional students to receive Direct PLUS loans and sets the aggregate limit on unsubsidized loans to $65,000 for a graduate student. While the bill was referred to the Committee on Health, Education, Labor, and Pensions, it has yet to proceed. Even though neither bill targeting Grad PLUS loans has passed, they each signal lawmakers’ appetite for reforming graduate lending. That means potential changes to how students finance advanced degrees. What Grad PLUS Loan News Means for Borrowers As policymakers debate the future of federal student aid, Grad PLUS loans are undeniably on the chopping block. For current and prospective graduate students, that adds another layer of uncertainty to an already stressful financial climate. Rising tuition costs and fewer affordable borrowing options could leave many students scrambling to cover expenses. Finding student loans for graduate school, including from private lenders, will become more necessary for students who’ve exhausted free financial aid options. Current Grad PLUS Borrowers Students already enrolled or recent graduates with active Grad PLUS loans probably won’t see major changes, at least in the short term. If Congress eliminates the program, existing borrowers will likely be “grandfathered” in, meaning they can keep their current loans and repayment terms as they are. The uncertainty around the Grad PLUS loan 2024-2025 cycle could complicate financial planning for those midway through multi-year programs. If you’re in either of these groups, pay close attention to Grad PLUS loan news developments and start researching backup funding strategies in case future borrowing under Grad PLUS is capped or phased out. Future Grad PLUS Borrowers Future graduate students might be at bigger risk of losing out on Grad PLUS funding. If this federal loan program is eliminated, students may need to rely more heavily on private loans to finance their education. While private loans are just as effective at funding advanced degrees and may offer additional benefits like access to career readiness tools, they may also come with tighter credit requirements, variable interest rates, and other considerations—so it is important to compare your options. This shift from federal to private loans could disproportionately impact students with limited or poor credit histories. As a result, some may delay graduate studies, choose lower-cost institutions, or seek employer-sponsored education benefits. Others may turn to part-time enrollment or work full-time when studying, lengthening the time needed to complete a degree. If you’re thinking about attending grad school, now is the time to start preparing: Compare graduate program costs and consider how you might pay for your desired program if Grad PLUS loans go away. Research and apply for graduate scholarships, fellowships, and other grants. To do so, you’ll need to complete the Free Application for Federal Student Aid (FAFSA) every year. Apply for graduate assistantships or federal work-study programs. Availability of these programs may impact your school choice. Look into employer education benefits to help cover the cost of graduate school. Take steps to build a strong credit profile, research private loan terms, and prepare to borrow if you still need to cover costs. Ascent Is Here to Help We know that paying for grad school is an important concern for all students, and that Grad PLUS loans have been a vital resource. Even if they go away, however, there are still options. Try to be selective about your desired program, pursue all your options for free financial aid, and take your time comparing lenders for private student loans. Ascent can help you find the right loan terms and interest rate to support your graduate education, but we’re here for you beyond borrowing. Our resources for students and families offer guidance about paying for school, better budgeting, career-readiness, and more. Amid ongoing student loan changes, Ascent remains committed to empowering student success and financial wellness. FAQs What alternative loan options are available if the Grad PLUS ends? If Grad PLUS loans are phased out, future graduate students should first explore financial aid that doesn’t need to be repaid such as scholarships, fellowships, grants, graduate assistantships, work-study programs, and employer tuition reimbursement programs. If there are any gaps in funding, graduate students should consider federal unsubsidized loans and private student loans. Can private student loans cover the full cost of grad school? In many cases, private student loans can cover the full cost of attending graduate school, from tuition and fees to living expenses. Private loans have unique eligibility and loan limits determined by the lender, and they usually depend on your credit history or income. That makes planning and comparing loans from different providers a necessity. Will Grad PLUS loans be forgiven? Grad PLUS loans may be eligible for forgiveness under existing federal programs like the Public Service Loan Forgiveness (PSLF) or Income-Driven Repayment (IDR) plan forgiveness, provided you meet the necessary qualifications. However, there’s no separate forgiveness initiative specifically for Grad PLUS loans at this time. -

SAVE Payment Plan Blocked: What This Means for BorrowersStudent loan borrowers have a lot on their minds–and for good reason. Executive orders threatening the possible elimination of the Department of Education and a variety of other student loan changes introduce new disruptions to an already stressful situation. The 8th U.S. Circuit Court of Appeals’ recent decision to block the Biden administration’s SAVE Plan introduced even more uncertainty. Many borrowers on the Saving on Valuable Education (SAVE) Plan now find themselves in limbo, not paying on their loans or accruing interest, but not progressing toward loan forgiveness. Students, borrowers, and their families need to understand how recent decisions and actions by courts and Congress can impact their loans and repayment plans. Key Takeaways The 8th U.S. Circuit Court of Appeals upheld an injunction blocking the Biden administration’s Saving on Valuable Education (SAVE) Plan in February 2025, halting its implementation. The Biden administration created the SAVE Plan in 2023 as an income-driven repayment plan to streamline loan payments and forgiveness for many borrowers. As a result of the court’s decision, SAVE Plan enrollees currently have their loans in forbearance, with no payments due or interest accrued. On March 26, 2025, the U.S. Department of Education reopened applications for Income-Based Repayment (IBR), PAYE, and ICR plans. Ascent provides tools to help students understand the benefits and drawbacks of student loans, including how the cost of education can impact their chosen degree’s return on investment. Understanding the SAVE Plan and Court Actions The SAVE Plan is an income-driven repayment (IDR) program introduced by the Biden administration in 2023. It replaced the Obama-era program, which was formerly known as Revised Pay As You Earn (REPAYE). The goal of this plan was to lower monthly student loan payments and offer borrowers a faster path to forgiveness that considered their income and family size more heavily than previous plans. However, in February 2025, a federal court injunction prevented the U.S. Department of Education from implementing the SAVE Plan and parts of other IDR plans. As a result, IDR and online consolidation applications became temporarily unavailable. The legal challenges to the SAVE Plan have been ongoing, with the following key dates: August 2023: The SAVE Plan officially launched, replacing the REPAYE Plan. Borrowers could enroll to access lower monthly payments and interest protections. October 2023: Major elements of the SAVE Plan took effect, including an increased income exemption and a stoppage of unpaid interest growth for qualified borrowers. March 2024: Multiple Republican-led states challenged the SAVE Plan, arguing overreach of executive authority. July 2024: A preliminary injunction via a federal court blocked full implementation in July 2024. August 2024: The Supreme Court declined to fast-track an appeal, meaning the SAVE Plan remained blocked while litigation continued. February 2025: The 8th U.S. Circuit Court of Appeals upheld the injunction, citing concerns over the Education Department’s authority and potential financial impacts on states. The online IDR application is available again (as of March 26, 2025). Borrowers can still apply for Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR) plans. Loan consolidation is also available. What Happens to Borrowers Enrolled in the SAVE Plan? Borrowers on the SAVE Plan are directly impacted by these legal battles. Currently, SAVE Plan participants are placed into administrative forbearance; they’re not legally required to make monthly payments, and the interest on their loans won’t accrue. For those on a tight budget, that can be helpful. That said, forbearance isn’t forgiveness, and months spent in forbearance don’t count toward loan forgiveness programs like the Public Service Loan Forgiveness (PSLF) or traditional income-driven repayment forgiveness. The U.S. Department of Education expects this pause to continue until at least December 2025, unless court rulings change the situation. If you’re a borrower in forbearance, stay up to date on the status of your loans. Ensure your loan servicer has your up-to-date contact information, and check in with studentaid.gov for the latest student loan news. How Are Loan Forgiveness Options Affected? The SAVE Plan block greatly impacts loan forgiveness paths, including PSLF. Because enrolled borrowers are now in administrative forbearance, the months they spend without making payments don’t count toward the 120 qualifying payments for PSLF or the 20 to 25 years necessary for IDR forgiveness. That pause could delay borrowers’ progress unless future policy changes address the gap. SAVE Plan borrowers may want to explore alternative IDR plans like PAYE or IBR to stay on track toward PSLF or IDR forgiveness. Alternatively, if you’ve already completed 120 months of qualifying employment, the PSLF Buyback program lets you “buy back” certain months spent in forbearance, helping you stay on track toward loan forgiveness. Knowing what other repayment options are available can make a world of difference when managing student debt. What Will Happen to Other Income-Driven Repayment Plans? Given the news about the SAVE Plan, many borrowers might have concerns about other income-driven repayment options. As previously noted, the U.S. Department of Education has reopened applications for certain IDR plans, including IBR, PAYE, and ICR, as of March 26, 2025. Borrowers can now apply for or recertify these student loan repayment plans through the online application. However, the broader political climate around student loan reform suggests changes might be on the horizon. Future administrations or legislative actions could aim to retool or modernize IDR plans, especially if the SAVE Plan remains permanently blocked. Borrowers can prepare for any future changes by making proactive decisions: Stay enrolled in current IDR plans and continue making qualifying payments. Monitor official updates from the Department of Education for any policy changes. Explore alternatives if you’re nearing forgiveness milestones or need to adjust your payment strategy. Consult your loan servicer when uncertain about your plan’s status or your next steps. The biggest takeaway for any student loan borrower is to keep up with student loan news over the coming months, especially as the state of repayment and forgiveness programs continues to change. Considerations for Future Borrowers While following student loan news is important for current borrowers, it’s just as critical for future borrowers, students, and parents to stay up to date. Future college students should think carefully about how they will finance their education. The uncertainty of programs like the SAVE Plan and potential reforms to other IDR plans highlights why incoming students should prioritize grants, scholarships, and other financial aid whenever possible and consider the return on investment of their chosen degree. Completing the Free Application for Federal Student Aid (FAFSA) is a key step to financing education, even in the face of changes to federal loan programs. The FAFSA gauges loan eligibility and is often the only way to qualify for need-based Pell Grants, work-study jobs, and campus aid. Complete the FAFSA as early as possible to avoid missing out on potential aid opportunities. And before you take out student loans, use tools like our College Degree ROI Calculator to help estimate the average annual cost of a degree against the first-year salaries in your chosen field. Ascent Is Here to Help Understanding student loan repayment can help you avoid financial headaches, but it’s easy to feel overwhelmed by ongoing changes and shifting policy updates. Ascent is here to help. In addition to our variety of private student loans, we have a library of student success resources to support students and their families in college—and beyond. Plus, when you’re ready to jump-start your dream career, our AscentUP program can provide professional development training and coaching to help you build confidence and develop the skills you need for your next chapter. Check out our blog for more resources and information surrounding education, student loans, and financial wellness today. FAQs What happens now that the SAVE plan is blocked? Borrowers currently enrolled in the SAVE Plan have been placed in administrative forbearance. During this time, monthly payments are not required, and interest does not accrue. Borrowers should keep in mind that months spent in forbearance don’t count toward forgiveness programs, which might prolong the process of paying off your loans or having them forgiven. Why was the SAVE plan blocked? The SAVE Plan faced many legal challenges from Republican-led states, which argued that the Department of Education exceeded its authority in creating the program without congressional approval. On February 18, 2025, the 8th U.S. Circuit Court of Appeals upheld a preliminary injunction against the SAVE Plan, agreeing with the states that the plan's provisions—particularly those related to loan forgiveness—went beyond the Department of Education's statutory authority. Is there any chance the SAVE plan will be reinstated? Given the current political climate and other actions taken by the Trump administration, it’s unlikely that the SAVE Plan will be reinstated anytime soon. Can I still apply for income-driven repayment (IDR) plans like PAYE or IBR? Yes, you can still apply for certain income-driven repayment (IDR) plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR). Following a temporary suspension due to a court injunction in February 2025, the U.S. Department of Education reopened applications for these plans on March 26, 2025. Can private loans offer similar terms to what SAVE would’ve provided? Most private student loans do not offer the same payment structures or forgiveness options as federal programs like SAVE. That said, some private lenders offer forbearance or income-based options. Carefully compare terms before you refinance or choose a private student loan provider.

SAVE Payment Plan Blocked: What This Means for BorrowersStudent loan borrowers have a lot on their minds–and for good reason. Executive orders threatening the possible elimination of the Department of Education and a variety of other student loan changes introduce new disruptions to an already stressful situation. The 8th U.S. Circuit Court of Appeals’ recent decision to block the Biden administration’s SAVE Plan introduced even more uncertainty. Many borrowers on the Saving on Valuable Education (SAVE) Plan now find themselves in limbo, not paying on their loans or accruing interest, but not progressing toward loan forgiveness. Students, borrowers, and their families need to understand how recent decisions and actions by courts and Congress can impact their loans and repayment plans. Key Takeaways The 8th U.S. Circuit Court of Appeals upheld an injunction blocking the Biden administration’s Saving on Valuable Education (SAVE) Plan in February 2025, halting its implementation. The Biden administration created the SAVE Plan in 2023 as an income-driven repayment plan to streamline loan payments and forgiveness for many borrowers. As a result of the court’s decision, SAVE Plan enrollees currently have their loans in forbearance, with no payments due or interest accrued. On March 26, 2025, the U.S. Department of Education reopened applications for Income-Based Repayment (IBR), PAYE, and ICR plans. Ascent provides tools to help students understand the benefits and drawbacks of student loans, including how the cost of education can impact their chosen degree’s return on investment. Understanding the SAVE Plan and Court Actions The SAVE Plan is an income-driven repayment (IDR) program introduced by the Biden administration in 2023. It replaced the Obama-era program, which was formerly known as Revised Pay As You Earn (REPAYE). The goal of this plan was to lower monthly student loan payments and offer borrowers a faster path to forgiveness that considered their income and family size more heavily than previous plans. However, in February 2025, a federal court injunction prevented the U.S. Department of Education from implementing the SAVE Plan and parts of other IDR plans. As a result, IDR and online consolidation applications became temporarily unavailable. The legal challenges to the SAVE Plan have been ongoing, with the following key dates: August 2023: The SAVE Plan officially launched, replacing the REPAYE Plan. Borrowers could enroll to access lower monthly payments and interest protections. October 2023: Major elements of the SAVE Plan took effect, including an increased income exemption and a stoppage of unpaid interest growth for qualified borrowers. March 2024: Multiple Republican-led states challenged the SAVE Plan, arguing overreach of executive authority. July 2024: A preliminary injunction via a federal court blocked full implementation in July 2024. August 2024: The Supreme Court declined to fast-track an appeal, meaning the SAVE Plan remained blocked while litigation continued. February 2025: The 8th U.S. Circuit Court of Appeals upheld the injunction, citing concerns over the Education Department’s authority and potential financial impacts on states. The online IDR application is available again (as of March 26, 2025). Borrowers can still apply for Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR) plans. Loan consolidation is also available. What Happens to Borrowers Enrolled in the SAVE Plan? Borrowers on the SAVE Plan are directly impacted by these legal battles. Currently, SAVE Plan participants are placed into administrative forbearance; they’re not legally required to make monthly payments, and the interest on their loans won’t accrue. For those on a tight budget, that can be helpful. That said, forbearance isn’t forgiveness, and months spent in forbearance don’t count toward loan forgiveness programs like the Public Service Loan Forgiveness (PSLF) or traditional income-driven repayment forgiveness. The U.S. Department of Education expects this pause to continue until at least December 2025, unless court rulings change the situation. If you’re a borrower in forbearance, stay up to date on the status of your loans. Ensure your loan servicer has your up-to-date contact information, and check in with studentaid.gov for the latest student loan news. How Are Loan Forgiveness Options Affected? The SAVE Plan block greatly impacts loan forgiveness paths, including PSLF. Because enrolled borrowers are now in administrative forbearance, the months they spend without making payments don’t count toward the 120 qualifying payments for PSLF or the 20 to 25 years necessary for IDR forgiveness. That pause could delay borrowers’ progress unless future policy changes address the gap. SAVE Plan borrowers may want to explore alternative IDR plans like PAYE or IBR to stay on track toward PSLF or IDR forgiveness. Alternatively, if you’ve already completed 120 months of qualifying employment, the PSLF Buyback program lets you “buy back” certain months spent in forbearance, helping you stay on track toward loan forgiveness. Knowing what other repayment options are available can make a world of difference when managing student debt. What Will Happen to Other Income-Driven Repayment Plans? Given the news about the SAVE Plan, many borrowers might have concerns about other income-driven repayment options. As previously noted, the U.S. Department of Education has reopened applications for certain IDR plans, including IBR, PAYE, and ICR, as of March 26, 2025. Borrowers can now apply for or recertify these student loan repayment plans through the online application. However, the broader political climate around student loan reform suggests changes might be on the horizon. Future administrations or legislative actions could aim to retool or modernize IDR plans, especially if the SAVE Plan remains permanently blocked. Borrowers can prepare for any future changes by making proactive decisions: Stay enrolled in current IDR plans and continue making qualifying payments. Monitor official updates from the Department of Education for any policy changes. Explore alternatives if you’re nearing forgiveness milestones or need to adjust your payment strategy. Consult your loan servicer when uncertain about your plan’s status or your next steps. The biggest takeaway for any student loan borrower is to keep up with student loan news over the coming months, especially as the state of repayment and forgiveness programs continues to change. Considerations for Future Borrowers While following student loan news is important for current borrowers, it’s just as critical for future borrowers, students, and parents to stay up to date. Future college students should think carefully about how they will finance their education. The uncertainty of programs like the SAVE Plan and potential reforms to other IDR plans highlights why incoming students should prioritize grants, scholarships, and other financial aid whenever possible and consider the return on investment of their chosen degree. Completing the Free Application for Federal Student Aid (FAFSA) is a key step to financing education, even in the face of changes to federal loan programs. The FAFSA gauges loan eligibility and is often the only way to qualify for need-based Pell Grants, work-study jobs, and campus aid. Complete the FAFSA as early as possible to avoid missing out on potential aid opportunities. And before you take out student loans, use tools like our College Degree ROI Calculator to help estimate the average annual cost of a degree against the first-year salaries in your chosen field. Ascent Is Here to Help Understanding student loan repayment can help you avoid financial headaches, but it’s easy to feel overwhelmed by ongoing changes and shifting policy updates. Ascent is here to help. In addition to our variety of private student loans, we have a library of student success resources to support students and their families in college—and beyond. Plus, when you’re ready to jump-start your dream career, our AscentUP program can provide professional development training and coaching to help you build confidence and develop the skills you need for your next chapter. Check out our blog for more resources and information surrounding education, student loans, and financial wellness today. FAQs What happens now that the SAVE plan is blocked? Borrowers currently enrolled in the SAVE Plan have been placed in administrative forbearance. During this time, monthly payments are not required, and interest does not accrue. Borrowers should keep in mind that months spent in forbearance don’t count toward forgiveness programs, which might prolong the process of paying off your loans or having them forgiven. Why was the SAVE plan blocked? The SAVE Plan faced many legal challenges from Republican-led states, which argued that the Department of Education exceeded its authority in creating the program without congressional approval. On February 18, 2025, the 8th U.S. Circuit Court of Appeals upheld a preliminary injunction against the SAVE Plan, agreeing with the states that the plan's provisions—particularly those related to loan forgiveness—went beyond the Department of Education's statutory authority. Is there any chance the SAVE plan will be reinstated? Given the current political climate and other actions taken by the Trump administration, it’s unlikely that the SAVE Plan will be reinstated anytime soon. Can I still apply for income-driven repayment (IDR) plans like PAYE or IBR? Yes, you can still apply for certain income-driven repayment (IDR) plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR). Following a temporary suspension due to a court injunction in February 2025, the U.S. Department of Education reopened applications for these plans on March 26, 2025. Can private loans offer similar terms to what SAVE would’ve provided? Most private student loans do not offer the same payment structures or forgiveness options as federal programs like SAVE. That said, some private lenders offer forbearance or income-based options. Carefully compare terms before you refinance or choose a private student loan provider. -

Learn to Save Smart with Student DiscountsBalancing the costs of being a student can get complicated and expensive. Whether you’re worried about textbooks, rent, meals, or any other expenses, student discounts can help lighten the load. In this blog, we’ll shine light on some great discounts that companies offer for students like you. Remember, while saving money is a win, it’s still smart to stick to your budget—don’t overspend just because it’s a good deal! Technology As a college student, having access to technology is essential, but thisit can also get really costly. Let’s explore some discounts tech companies offer to students to help ease the cost. Apple Apple offers exclusive discounts not only for college students but also for parents, faculty, and staff. Enjoy special pricing on Macs, iPads, and select accessories. Microsoft Microsoft offers discounts for students and teachers. They offer discounts on their Surface laptops and access to Microsoft Teams, Word, Excel, PowerPoint, and more for free. With your student email, it is available until you graduate. Dell You can create a free Dell Rewards account with your email and get savings after getting verified as a college student. Their rewards system allows you to get cash back to put towards your future Dell.com purchases. HP HP’s online education store offers up to 40% as part of their membership benefits. This includes discounts on laptops, desktops, accessories and printers. Streaming Spotify It’s always nice to have some music, a podcast, or an audio book to get you through the day as a student. Spotify offers 50% off their premium monthly subscription for students. All you have to do is verify your college student enrollment with the SheerID verification form. You can also bundle this subscription with Hulu for even more savings! HBO Max Looking for a movie or show to watch between your study breaks and free time? Max offers students a 50% off discount for their streaming services. Apple Music Apple Music has got you covered with music, radio stations, and a discount too. Whether you are earning your associate, bachelor’s or postgraduate degree, you can get a special rate made just for students. Going out Piada One reason you should keep your student ID on you: Piada’s student special! You can get any sized entree and a large fountain drink for just $9, every day from 2-5pm, and all day on Wednesdays. Cinemark & AMC Looking to catch the latest blockbuster? Take a break from studying and check out nearby Cinemark theatre to see if they offer student discounts! You can enjoy special pricing with your student ID. Other theaters like AMC also provide student discounts, so don’t forget to ask about those deals too! Museum Discounts Whether you are traveling, or considering being a tourist in your own college town,, always call or check local museum websites for student deals. Some offer free hours or discounted prices with your student ID! Bank of America also offers free admission at participating museums to cardholders during the first weekend of every month . Ascent We offer great benefits to help students earn cash and savings too! Get a discount on your student loan when you enroll in automatic payments. When you sign up, you can save money with the 0.25%-1.00%* autopay discount. Not only are you getting the discount, but you won’t have to worry about missing any payments! Plus, it takes as little as $1 per month to qualify. Ascent student graduates get 1% of their total loan amount back in cash with our graduation reward**. We are proud of your accomplishment and want to celebrate you! Refer a friend and earn big! Recommend your friends to Ascent and you can earn an Amazon.com Gift Card for each friend you refer ***. The more you refer, the more you can earn. The more friends you refer, the more you can earn—everyone wins. Additional Sources There are also other resources like Student Beans and UNiDAYS where they give students access to more exclusive offers. After you've signed up and verified your student status, you unlock access to discounts for travel, food, clothing, and more! Conclusion Don’t miss out on any student discounts and benefits, a little can go a long way. Saving on technology, entertainment, and dining out can help you save extra money to put away for your expenses during your time in school. Take advantage of your student ID, make smart financial decisions, and be on the lookout for ways you can save for the future and set yourself up for success. * The final ACH discount approved depends on the borrower’s credit history, verifiable cost of attendance, and is subject to credit approval and verification of application information. Automatic Payment Discount of 0.25% is for credit-based loans and a 1.00% discount is for outcomes-based loans when you enroll in automatic payments. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. ** Ascent’s 1% Cash Back Graduation Reward is for eligible college students only and subject to terms and conditions. Eligible students must request the graduation reward from Ascent. Aggregate cash back limit of $500. Learn more at AscentFunding.com/CashBack. *** Refer a Friend program is subject to terms and conditions, click here for official rules and eligibility. Restrictions apply, see amazon.com/gc-legal Ascent Written, Native Advertising Disclosure Ascent Funding, LLC (“Ascent”) sponsors these blog posts and creates informational content that is of interest to prospective borrowers and our applicants. The information included in this blog post could include technical or other inaccuracies or typographical errors. It is solely your responsibility to evaluate the accuracy, completeness and usefulness of all opinions, advice, services, merchandise and other information provided herein. ASCENT IS NOT RESPONSIBLE FOR, AND EXPRESSLY DISCLAIMS ALL LIABILITY FOR, DAMAGES OF ANY KIND ARISING OUT OF USE, REFERENCE TO, OR RELIANCE ON ANY INFORMATION CONTAINED WITHIN THESE BLOG POSTS (INCLUDING THIRD-PARTY SITES). ASCENT OFFERS LINKS TO THIRD PARTY WEBSITES AND ARTICLES SOLELY FOR INFORMATIONAL PURPOSES. WHEN YOU CLICK ON THESE LINKS YOU WILL LEAVE THE ASCENT WEBSITE AND WILL BE REDIRECTED TO ANOTHER SITE. THESE SITES ARE NOT UNDER THE DIRECTION OR CONTROL OF ASCENT. WE ARE NOT AN AGENT FOR THESE THIRD PARTIES NOR DO WE ENDORSE OR GUARANTEE THEIR PRODUCTS OR THEIR WEBSITE CONTENT. ASCENT MAKES NO REPRESENTATIONS REGARDING THE SUITABILITY OR ACCURACY OF THE CONTENT IN SUCH SITES AND WE ARE NOT RESPONSIBLE FOR ANY OF THE CONTENT OF LINKED THIRD PARTY WEBSITES. As current and former students, we provide free resources to help you throughout your education, which may include links to third-party websites (where security and privacy policies may differ from Ascent’s). For our full disclaimer, please click here.

Learn to Save Smart with Student DiscountsBalancing the costs of being a student can get complicated and expensive. Whether you’re worried about textbooks, rent, meals, or any other expenses, student discounts can help lighten the load. In this blog, we’ll shine light on some great discounts that companies offer for students like you. Remember, while saving money is a win, it’s still smart to stick to your budget—don’t overspend just because it’s a good deal! Technology As a college student, having access to technology is essential, but thisit can also get really costly. Let’s explore some discounts tech companies offer to students to help ease the cost. Apple Apple offers exclusive discounts not only for college students but also for parents, faculty, and staff. Enjoy special pricing on Macs, iPads, and select accessories. Microsoft Microsoft offers discounts for students and teachers. They offer discounts on their Surface laptops and access to Microsoft Teams, Word, Excel, PowerPoint, and more for free. With your student email, it is available until you graduate. Dell You can create a free Dell Rewards account with your email and get savings after getting verified as a college student. Their rewards system allows you to get cash back to put towards your future Dell.com purchases. HP HP’s online education store offers up to 40% as part of their membership benefits. This includes discounts on laptops, desktops, accessories and printers. Streaming Spotify It’s always nice to have some music, a podcast, or an audio book to get you through the day as a student. Spotify offers 50% off their premium monthly subscription for students. All you have to do is verify your college student enrollment with the SheerID verification form. You can also bundle this subscription with Hulu for even more savings! HBO Max Looking for a movie or show to watch between your study breaks and free time? Max offers students a 50% off discount for their streaming services. Apple Music Apple Music has got you covered with music, radio stations, and a discount too. Whether you are earning your associate, bachelor’s or postgraduate degree, you can get a special rate made just for students. Going out Piada One reason you should keep your student ID on you: Piada’s student special! You can get any sized entree and a large fountain drink for just $9, every day from 2-5pm, and all day on Wednesdays. Cinemark & AMC Looking to catch the latest blockbuster? Take a break from studying and check out nearby Cinemark theatre to see if they offer student discounts! You can enjoy special pricing with your student ID. Other theaters like AMC also provide student discounts, so don’t forget to ask about those deals too! Museum Discounts Whether you are traveling, or considering being a tourist in your own college town,, always call or check local museum websites for student deals. Some offer free hours or discounted prices with your student ID! Bank of America also offers free admission at participating museums to cardholders during the first weekend of every month . Ascent We offer great benefits to help students earn cash and savings too! Get a discount on your student loan when you enroll in automatic payments. When you sign up, you can save money with the 0.25%-1.00%* autopay discount. Not only are you getting the discount, but you won’t have to worry about missing any payments! Plus, it takes as little as $1 per month to qualify. Ascent student graduates get 1% of their total loan amount back in cash with our graduation reward**. We are proud of your accomplishment and want to celebrate you! Refer a friend and earn big! Recommend your friends to Ascent and you can earn an Amazon.com Gift Card for each friend you refer ***. The more you refer, the more you can earn. The more friends you refer, the more you can earn—everyone wins. Additional Sources There are also other resources like Student Beans and UNiDAYS where they give students access to more exclusive offers. After you've signed up and verified your student status, you unlock access to discounts for travel, food, clothing, and more! Conclusion Don’t miss out on any student discounts and benefits, a little can go a long way. Saving on technology, entertainment, and dining out can help you save extra money to put away for your expenses during your time in school. Take advantage of your student ID, make smart financial decisions, and be on the lookout for ways you can save for the future and set yourself up for success. * The final ACH discount approved depends on the borrower’s credit history, verifiable cost of attendance, and is subject to credit approval and verification of application information. Automatic Payment Discount of 0.25% is for credit-based loans and a 1.00% discount is for outcomes-based loans when you enroll in automatic payments. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. ** Ascent’s 1% Cash Back Graduation Reward is for eligible college students only and subject to terms and conditions. Eligible students must request the graduation reward from Ascent. Aggregate cash back limit of $500. Learn more at AscentFunding.com/CashBack. *** Refer a Friend program is subject to terms and conditions, click here for official rules and eligibility. Restrictions apply, see amazon.com/gc-legal Ascent Written, Native Advertising Disclosure Ascent Funding, LLC (“Ascent”) sponsors these blog posts and creates informational content that is of interest to prospective borrowers and our applicants. The information included in this blog post could include technical or other inaccuracies or typographical errors. It is solely your responsibility to evaluate the accuracy, completeness and usefulness of all opinions, advice, services, merchandise and other information provided herein. ASCENT IS NOT RESPONSIBLE FOR, AND EXPRESSLY DISCLAIMS ALL LIABILITY FOR, DAMAGES OF ANY KIND ARISING OUT OF USE, REFERENCE TO, OR RELIANCE ON ANY INFORMATION CONTAINED WITHIN THESE BLOG POSTS (INCLUDING THIRD-PARTY SITES). ASCENT OFFERS LINKS TO THIRD PARTY WEBSITES AND ARTICLES SOLELY FOR INFORMATIONAL PURPOSES. WHEN YOU CLICK ON THESE LINKS YOU WILL LEAVE THE ASCENT WEBSITE AND WILL BE REDIRECTED TO ANOTHER SITE. THESE SITES ARE NOT UNDER THE DIRECTION OR CONTROL OF ASCENT. WE ARE NOT AN AGENT FOR THESE THIRD PARTIES NOR DO WE ENDORSE OR GUARANTEE THEIR PRODUCTS OR THEIR WEBSITE CONTENT. ASCENT MAKES NO REPRESENTATIONS REGARDING THE SUITABILITY OR ACCURACY OF THE CONTENT IN SUCH SITES AND WE ARE NOT RESPONSIBLE FOR ANY OF THE CONTENT OF LINKED THIRD PARTY WEBSITES. As current and former students, we provide free resources to help you throughout your education, which may include links to third-party websites (where security and privacy policies may differ from Ascent’s). For our full disclaimer, please click here. -